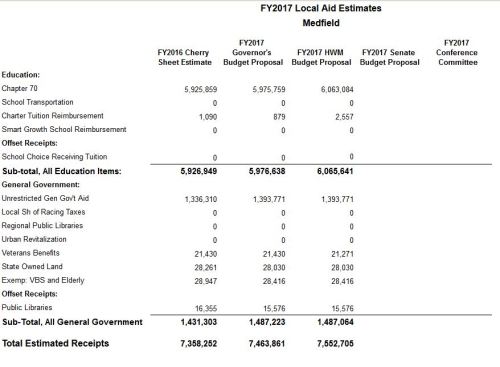

The House released its proposed budget numbers, and we do about $200,000 better than last year with their proposal. The Governor gave us about $100,000 more than last year. Usually our numbers do not go down, and the Senate which weighs in last often increases our total state aid. The Governor did revenue sharing by increasing part of our state aid by the same 4.3% that the state’s revenues increased, and the House extends that 4.3% increase to more state aid items. I am not sure why our Charter Tuition Reimbursement has gone up so much on a percentage basis.

Below is the report and instant analysis from the MMA yesterday afternoon on the state budget as it affects municipalities.

Wednesday, April 13, 2016

HOUSE BUDGET COMMITTEE OFFERS $39.5B FY 2017 STATE BUDGET THAT MAKES KEY INVESTMENTS IN MUNICIPAL AND SCHOOL AID

• INCLUDES THE FULL $42M INCREASE IN UNRESTRICTED MUNICIPAL AID (UGGA)

• INCREASES CHAPTER 70 BY $24M TO FUND MINIMUM AID AT $55 PER STUDENT

•ADDS A $10M RESERVE TO AID COMMUNITIES WITH LOW-INCOME STUDENTS

• ADDS $5M TO FUND THE SPECIAL EDUCATION CIRCUIT BREAKER

• ADDS $1M MORE FOR REGIONAL SCHOOL TRANSPORTATION

• LEVEL-FUNDS MOST OTHER MUNICIPAL AND SCHOOL ACCOUNTS

Earlier this afternoon, the House Ways and Means Committee reported out a lean $39.5 billion fiscal 2017 state budget plan to increase overall state expenditures by 3.3 percent. The House Ways and Means budget is $76 million smaller than the budget filed by the Governor in March, yet it also increases Chapter 70 aid by $24 million above the Governor’s recommendation by increasing minimum aid from $20 per student to $55 per student, and also includes a new $10 million reserve to aid communities impacted by changes in the calculations used to account for low-income students. The full House will debate the fiscal 2017 state budget during the week of April 25.

H. 4200, the House Ways and Means budget, provides strong progress on many important local aid priorities, including the full $42 million increase in Unrestricted General Government Aid that the Governor proposed and communities are counting on. The House W&M Committee would increase funding for several major aid programs, by adding $5 million to the Special Education Circuit Breaker, adding $1 million to Regional School Transportation, and increasing Chapter 70 minimum aid to $55 per student.

$42 MILLION INCREASE IN UNRESTRICTED MUNICIPAL AID

In a major victory for cities and towns, H. 4200 (the HW&M fiscal 2017 budget plan) would provide $1.021 billion for UGGA, a $42 million increase over current funding – the same increase proposed by Governor Baker. The $42 million would increase UGGA funding by 4.3 percent, which matches the growth in state tax collections next year. This would be the largest increase in discretionary municipal aid in nearly a decade. Every city and town would see their UGGA funding increase by 4.3 percent.

CHAPTER 70 MINIMUM AID WOULD INCREASE TO $55 PER STUDENT

The House budget committee is proposing a $95.8 million increase in Chapter 70 education aid, with a provision providing every city, town and school district an increase of at least $55 per student. This is $24 million more than the recommendation in the Governor’s budget submission. The budget would continue to implement the target share provisions enacted in 2007. Because most cities and towns only receive minimum aid, this increase would benefit the vast majority of communities.

FUNDS A $10M RESERVE TO AID COMMUNITIES WITH LOW-INCOME STUDENTS

The House Ways & Means budget also includes a new $10 million reserve to aid communities impacted by changes in the calculations used to account for low-income students. This would supplement Chapter 70 distributions to address shortfalls in aid levels due to the new methodology used to count low-income students. DESE would administer this program, and make funding decisions by October 2016.

$5 MILLION INCREASE INTENDED TO FULLY FUND SPECIAL EDUCATION CIRCUIT BREAKER

In another victory for cities and towns, House leaders have announced that they support full funding for the Special Education Circuit Breaker program. Their budget plan would provide $276.7 million, a $5 million increase above fiscal 2016, with the intention of fully funding the account. This is a vital program that every city, town and school district relies on to fund state-mandated services.

ADDS $1 MILLION TO REGIONAL SCHOOL TRANSPORTATION

House Ways and Means Committee budget would add $1 million to bring regional transportation reimbursements up to $60 million. The MMA will work to continue building on this welcome increase.

FUNDING FOR CHARTER SCHOOL REIMBURSEMENTS INCREASED BY $5 MILLION, BUT STILL UNDERFUNDED

Under state law, cities and towns that host or send students to charter schools are entitled to be reimbursed for a portion of their lost Chapter 70 aid. The state fully funded the reimbursement program in fiscal years 2013 and 2014, but is underfunding reimbursements by approximately $46.5 million this year. The House Ways and Means budget would increase funding for charter school reimbursements to $85.5 million, a $5 million boost, although this is $15 million less than the amount recommended by Gov. Baker. The program is underfunded in both budget proposals, and increasing this account will be a top priority during the budget debate.

PAYMENTS-IN-LIEU-OF-TAXES (PILOT), LIBRARY AID ACCOUNTS, METCO, McKINNEY-VENTO, AND SHANNON ANTI-GANG GRANTS

The House budget committee’s proposal would level-fund PILOT payments at $26.77 million, continue to fund library grant programs at $18.83 million, level-fund METCO $20.1 million, and level-fund McKinney-Vento reimbursements at $8.35 million. All four of these accounts are funded the same in both the Governor’s and House Ways and Means Committee’s budgets. However, the HW&M budget would reduce Shannon Anti-Gang Grants to $5 million, a $2 million reduction.

Please Call Your Representatives Today to Thank Them for the Strong Local Aid Investments in the House Ways and Means Committee Budget – Including the $42 Million Increase in Unrestricted Local Aid, Providing Chapter 70 Minimum Aid at $55 Per Student, Funding the Special Education Circuit Breaker, and Adding Funds to Regional School Transportation

Please Explain How the House Ways and Means Budget Impacts Your Community, and Ask Your Representatives to Build on this Progress During Budget Debate in the House

Thank You!