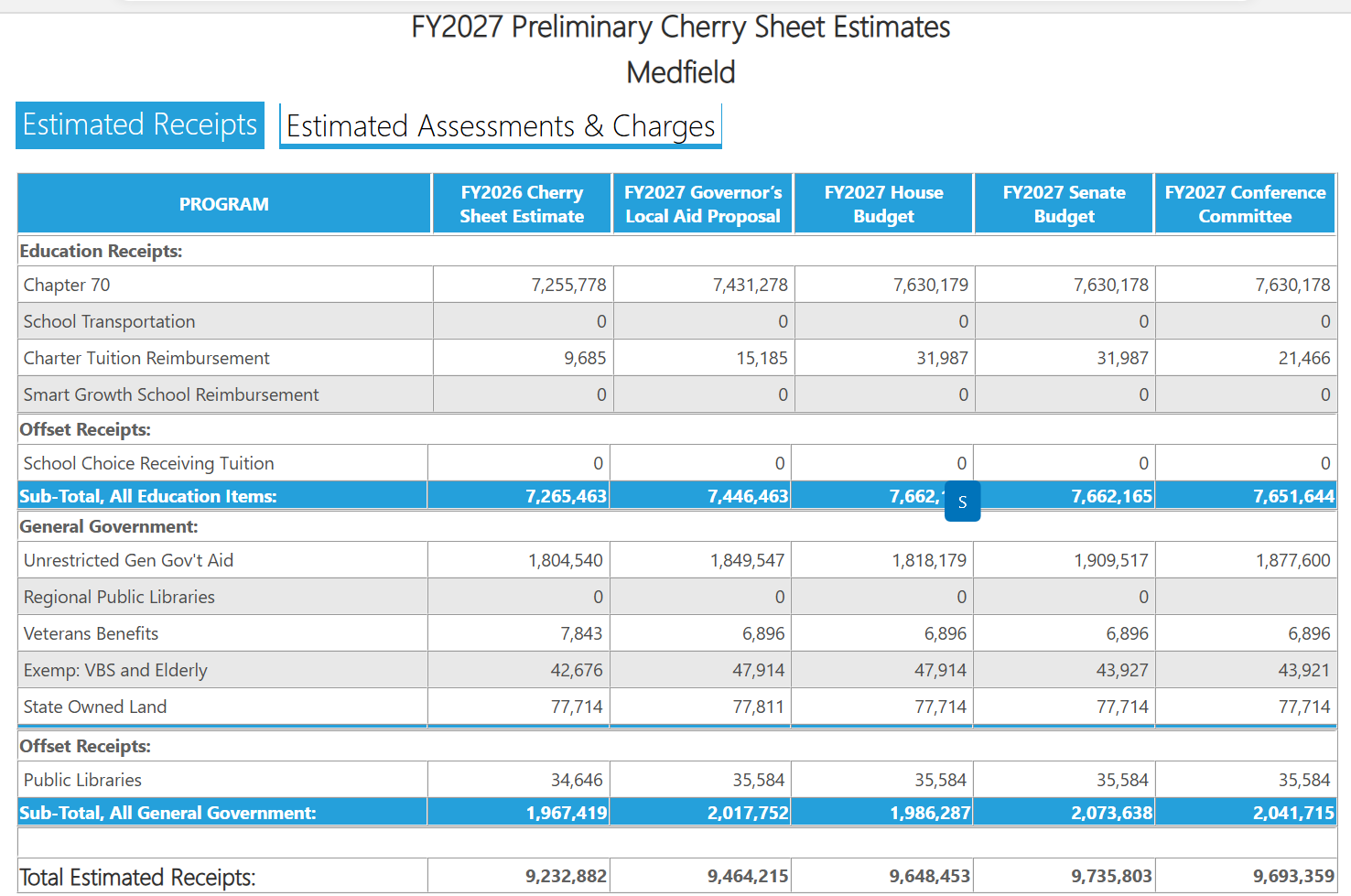

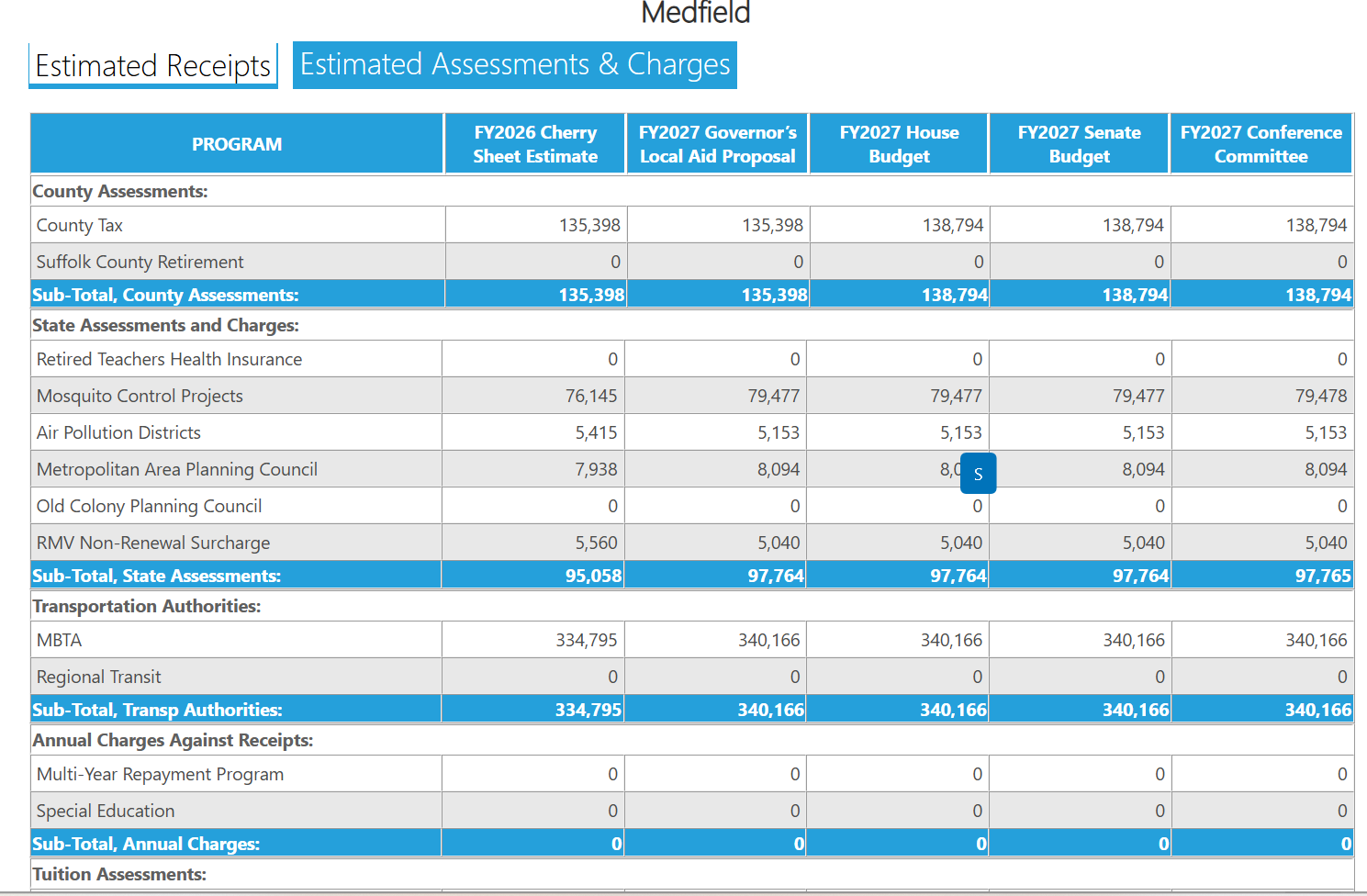

These are the Cherry Sheet numbers from the state budget that just passed. The town lost UGGA

These are the Cherry Sheet numbers from the state budget that just passed. The town lost UGGA

Comments Off on Medfield Lost ca. $40K total ($30K UGGA) in the state budget in Conference Committee

Posted in Budgets, Financial, Legislature, State

For further information click here –

WGBH article today says the Governor’s Municipal Empowerment bill that would have allowed towns to garner additional revenues has died in the legislature.

May 27, 2026

Gov. Maura Healey has tried twice to give cities and towns the ability to collect more revenue by raising some local taxes. State lawmakers have now rebuffed the idea for the second session in a row.

In January 2025, Healey filed legislation dubbed the Municipal Empowerment Act, intended to help local governments run more efficiently and tackle financial challenges. It was the second time she put forward a version of the bill, after the first version died the previous term without a vote in the Legislature.

The bill, among other measures, included sections that would let cities and towns adopt an extra surcharge on top of their existing motor vehicle excise taxes and increase local meals and lodging taxes in communities that have adopted those taxes. It wouldn’t require any municipality to raise taxes.

Comments Off on Legislature denies Medfield Right to Raise More Revenue

Posted in Budgets, Financial, Legislature, State

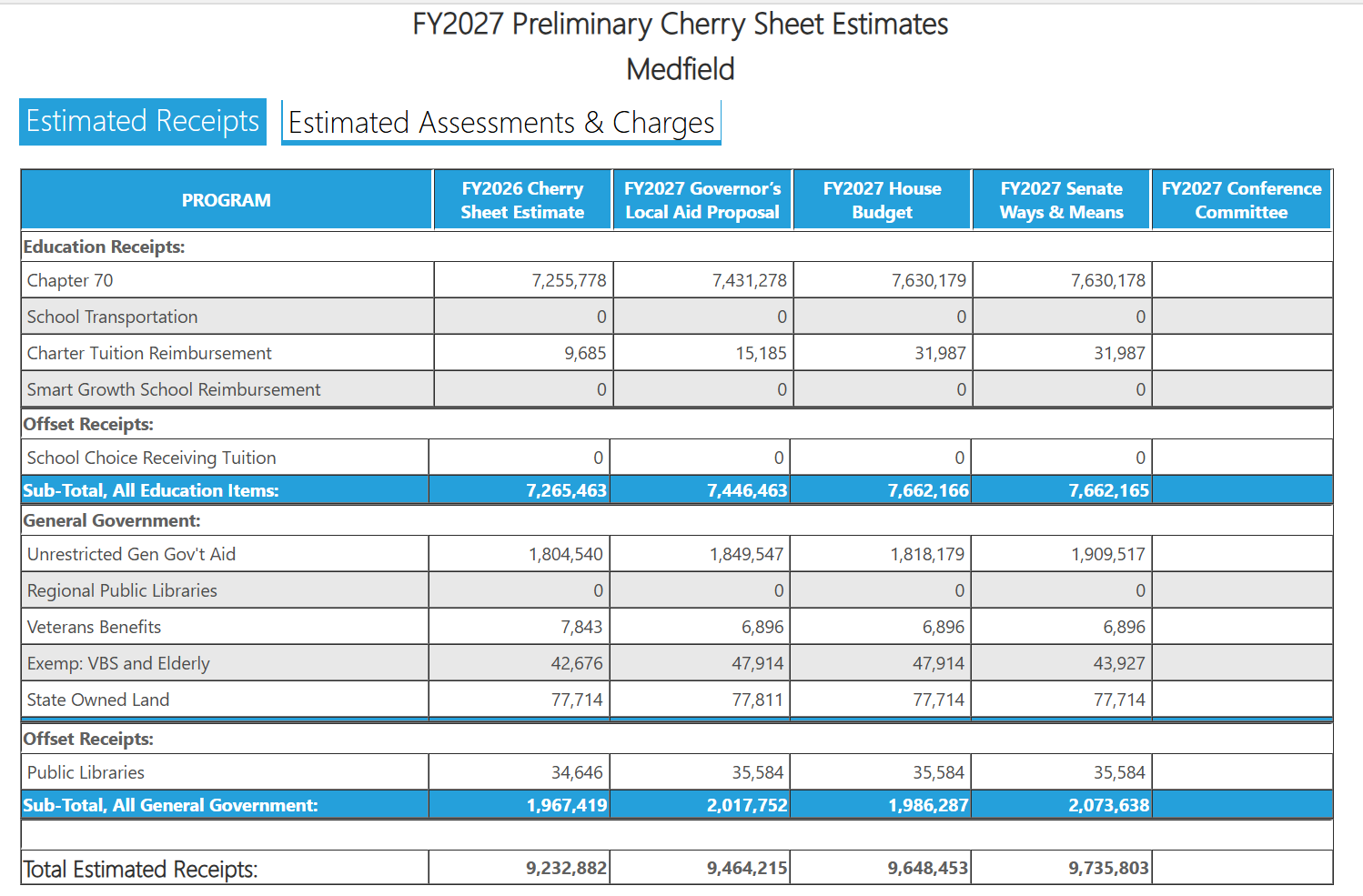

DOR has circulated the Cherry Sheets with the newly released Senate UGGA figures, in which Medfield gets about $60K more than in Gov’s version and about $90K more than in the House version:

Comments Off on Cherry Sheets – Senate adds $$$

Posted in Budgets, Financial, Legislature, State

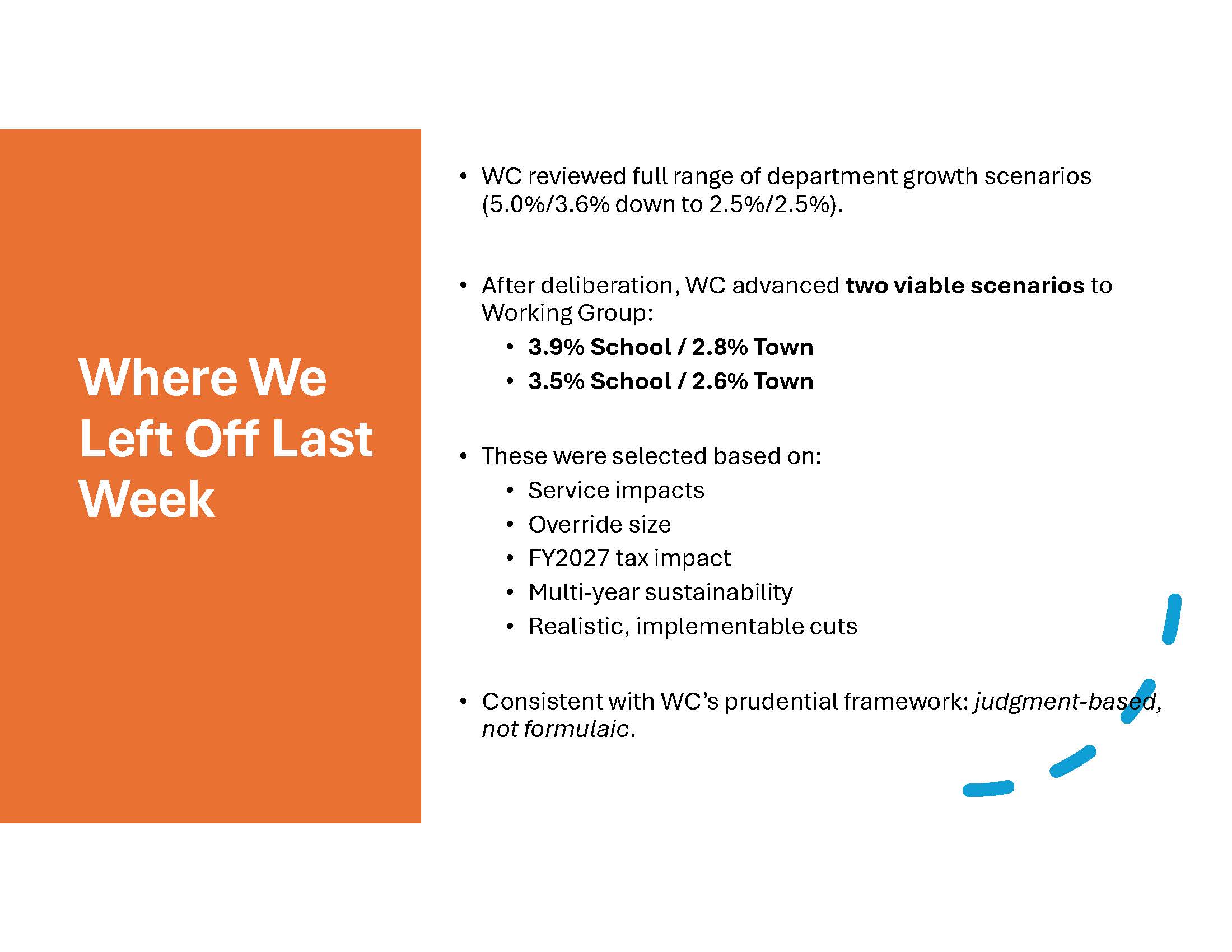

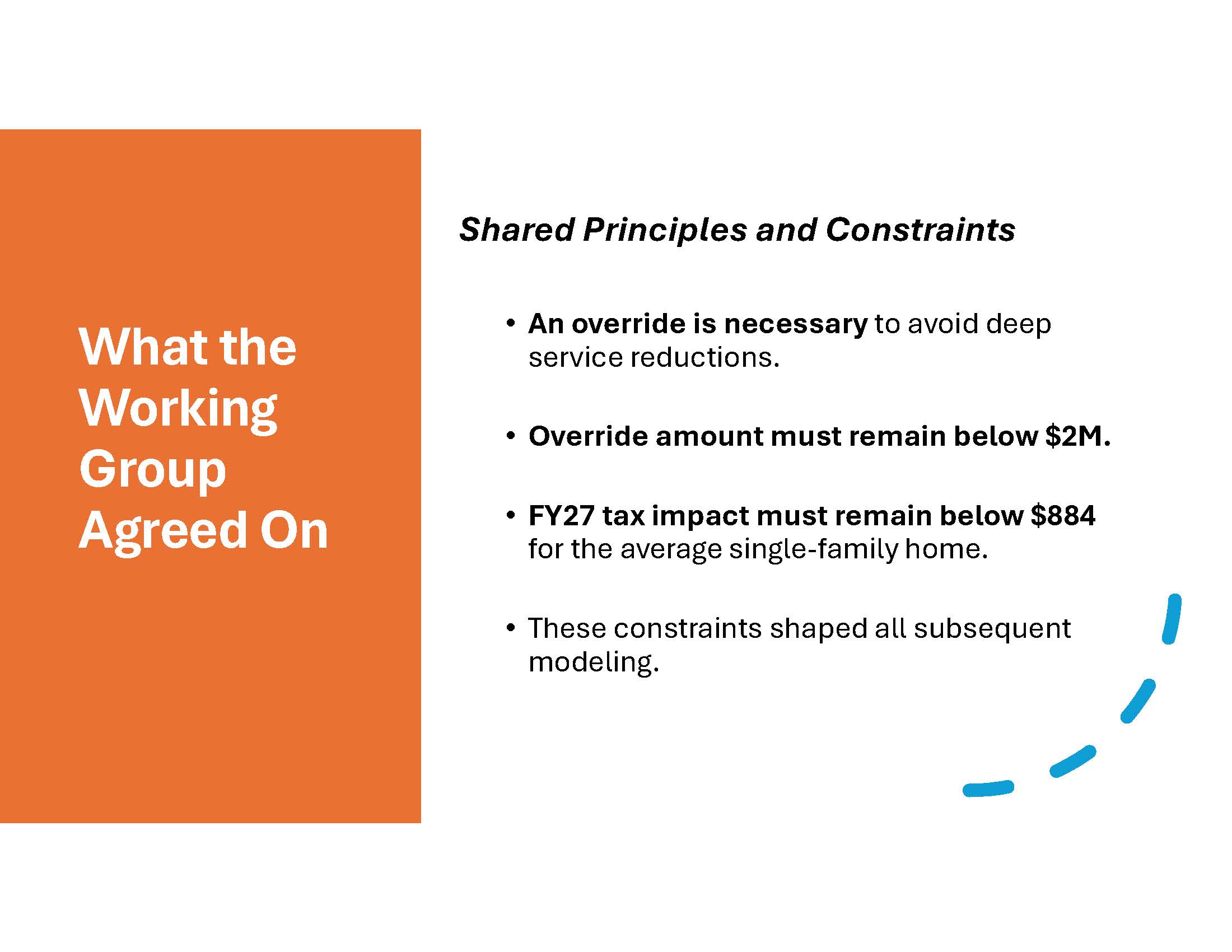

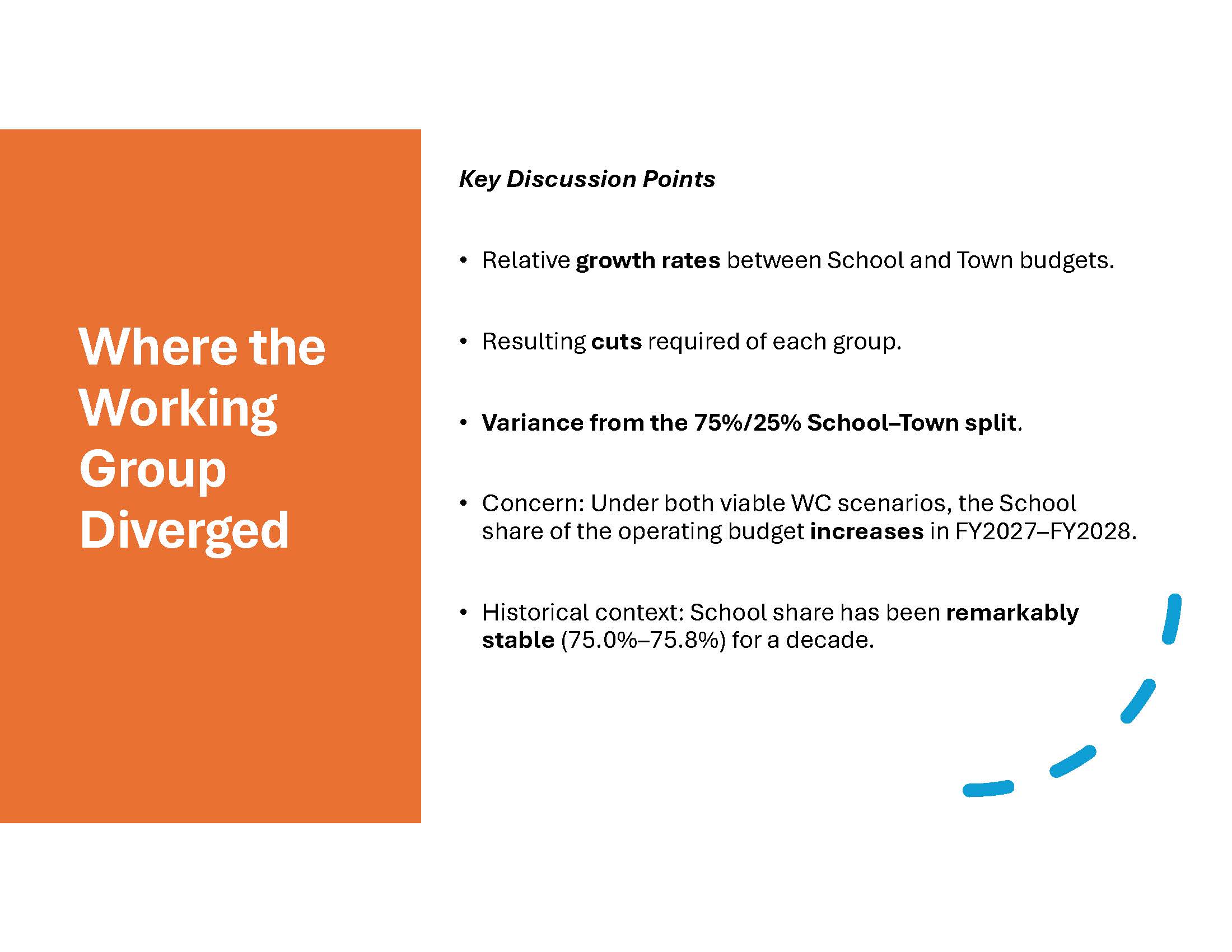

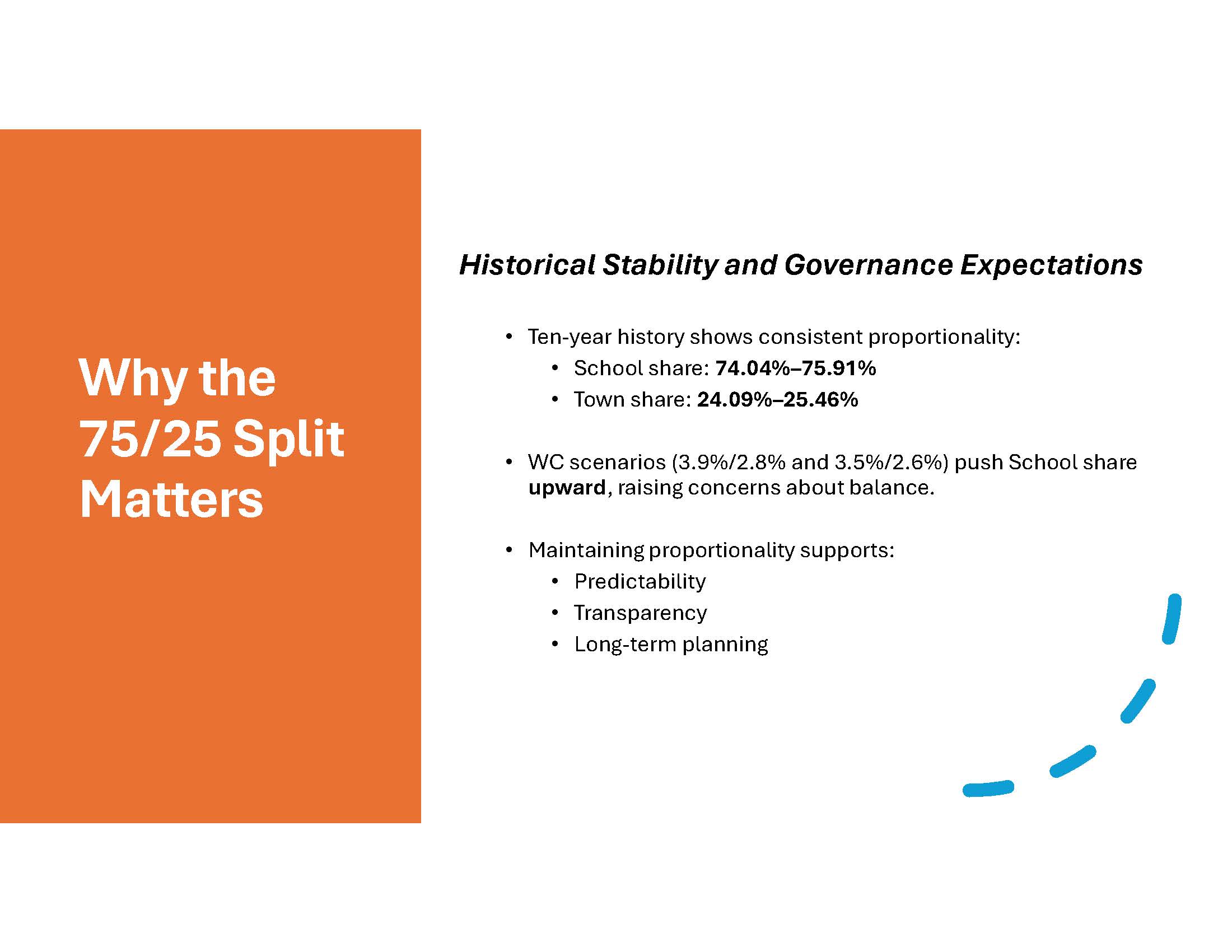

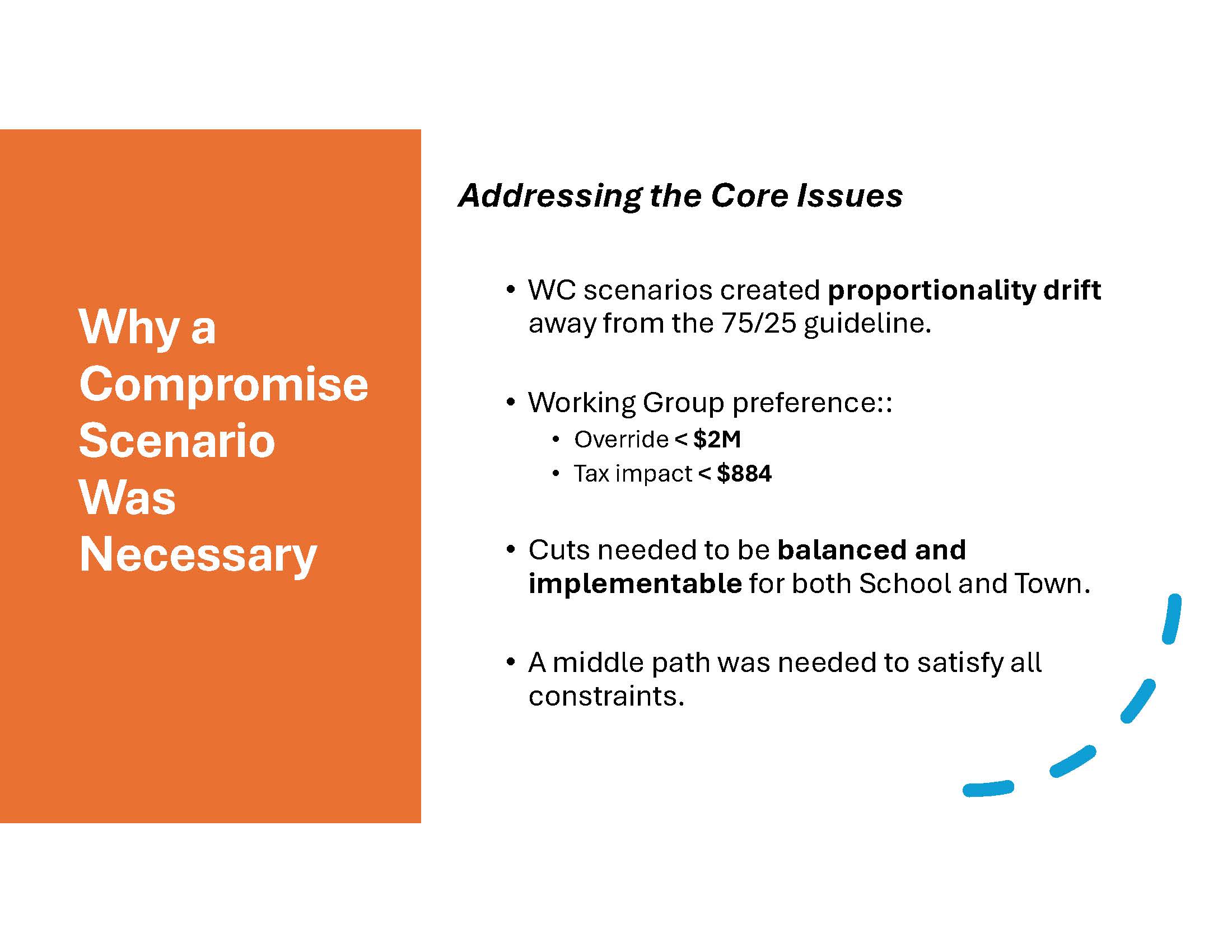

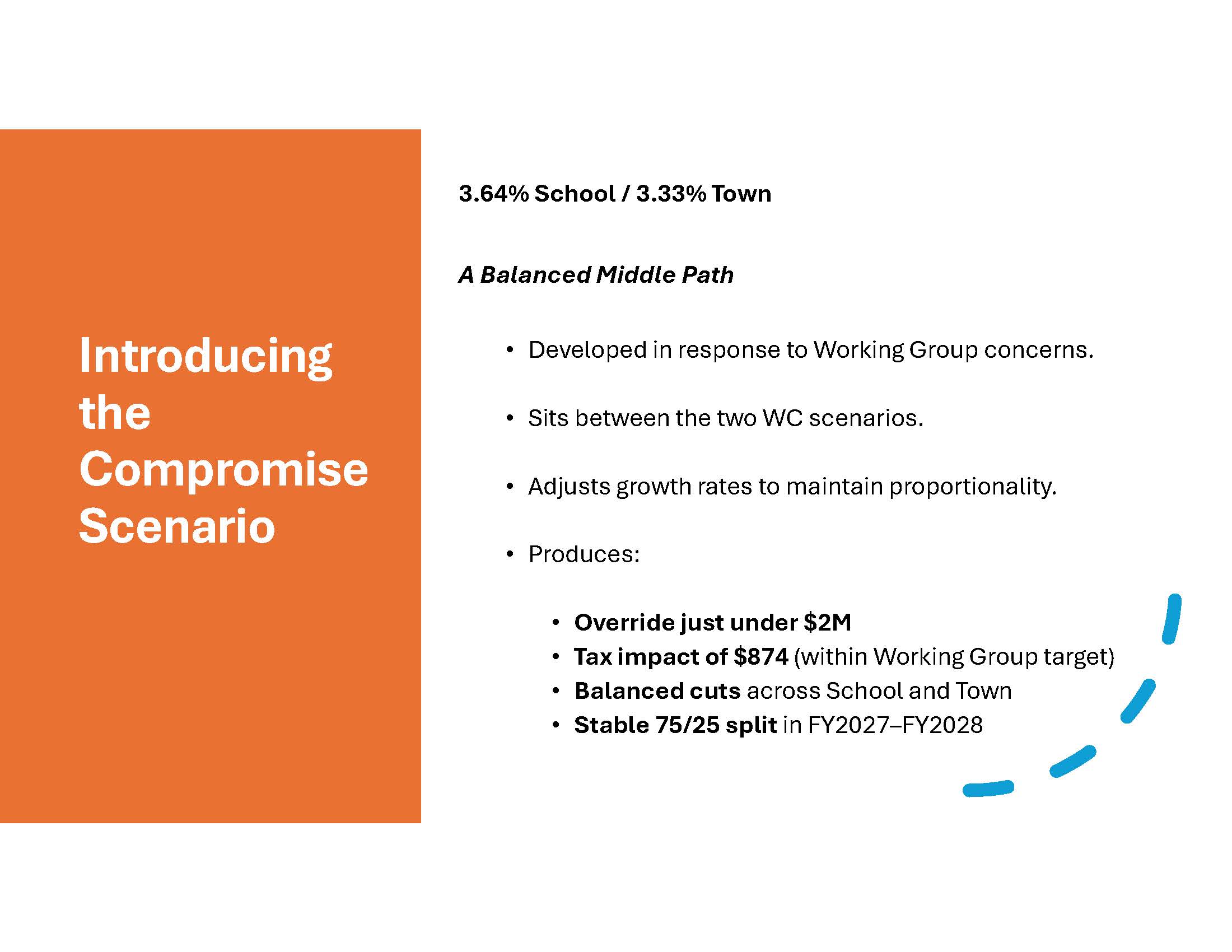

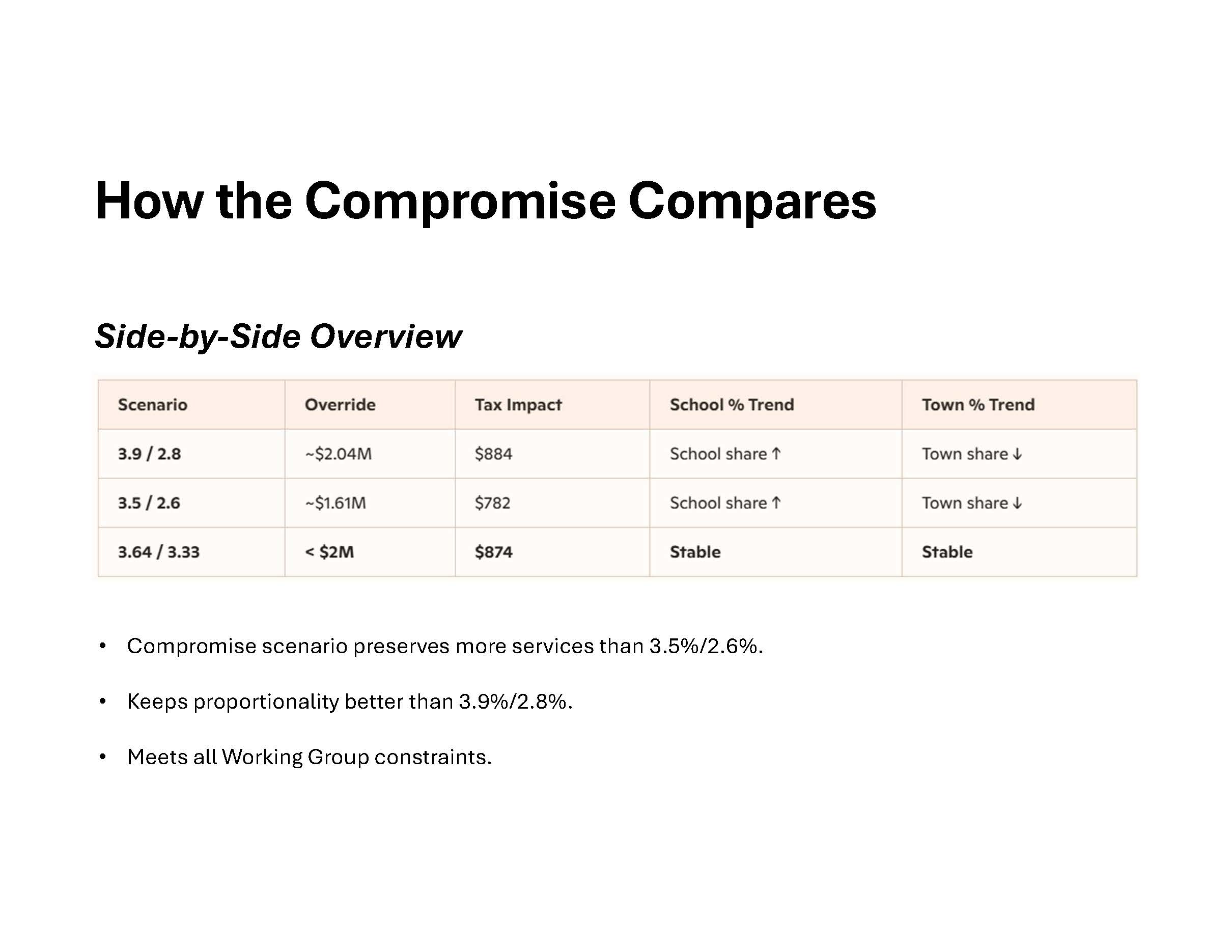

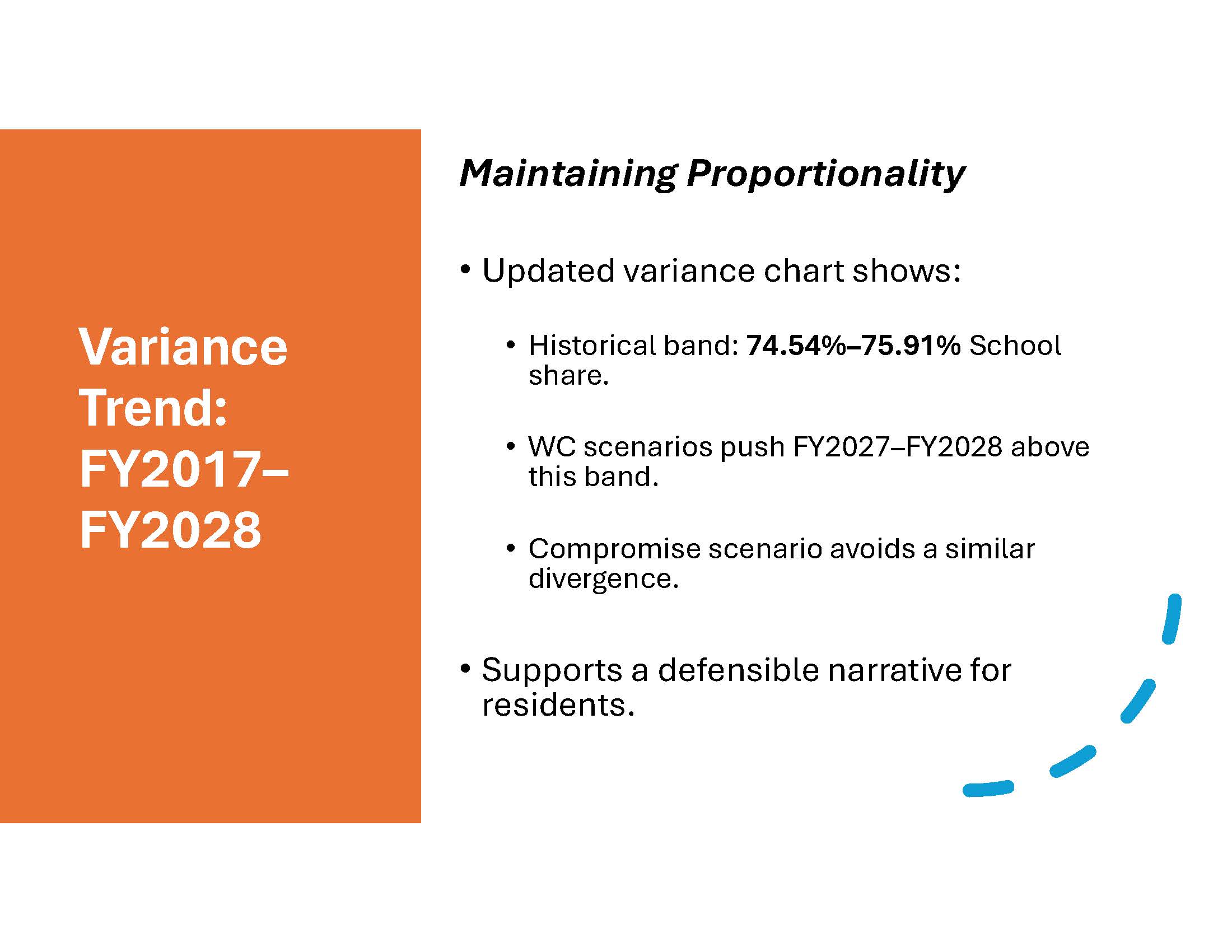

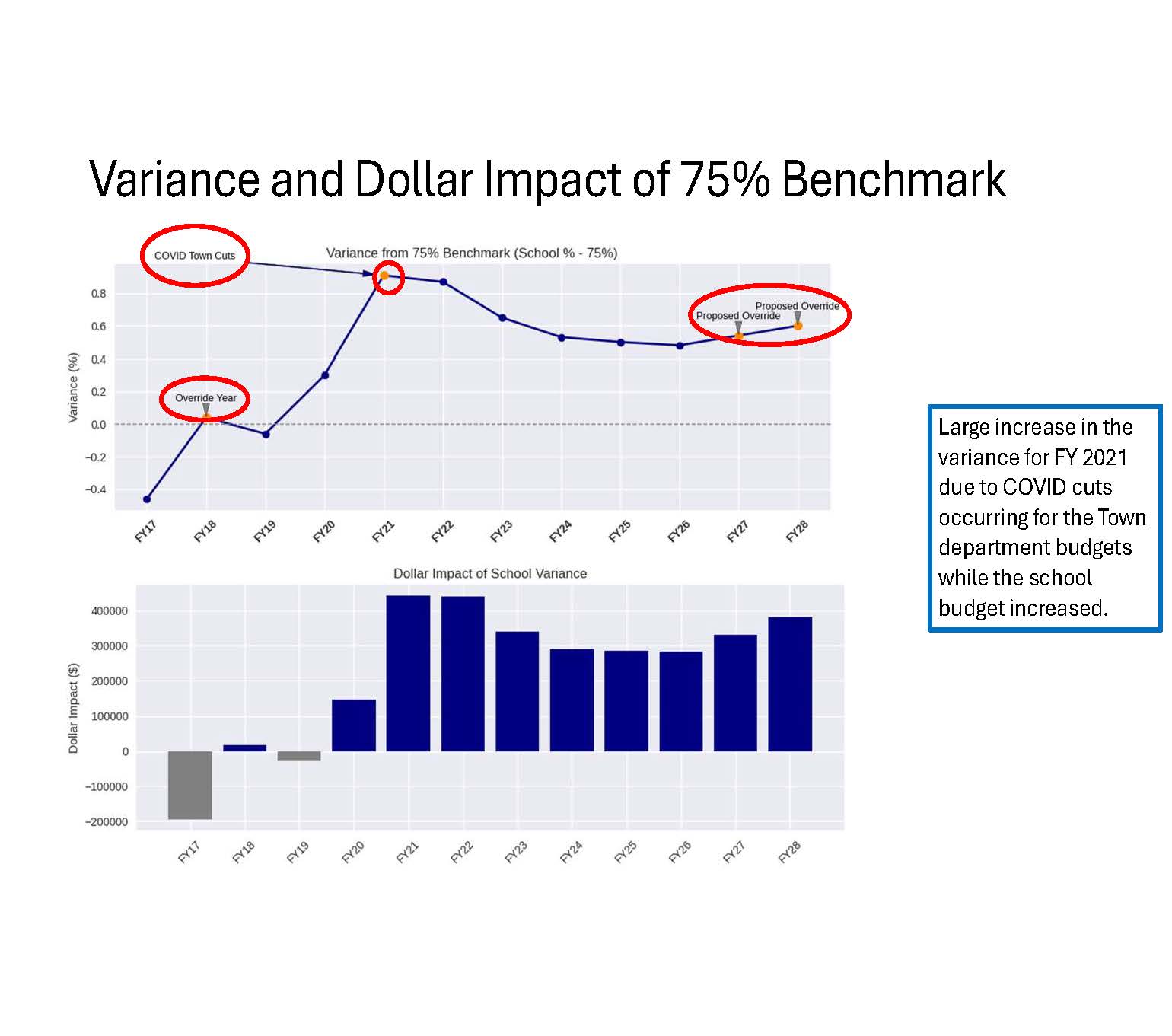

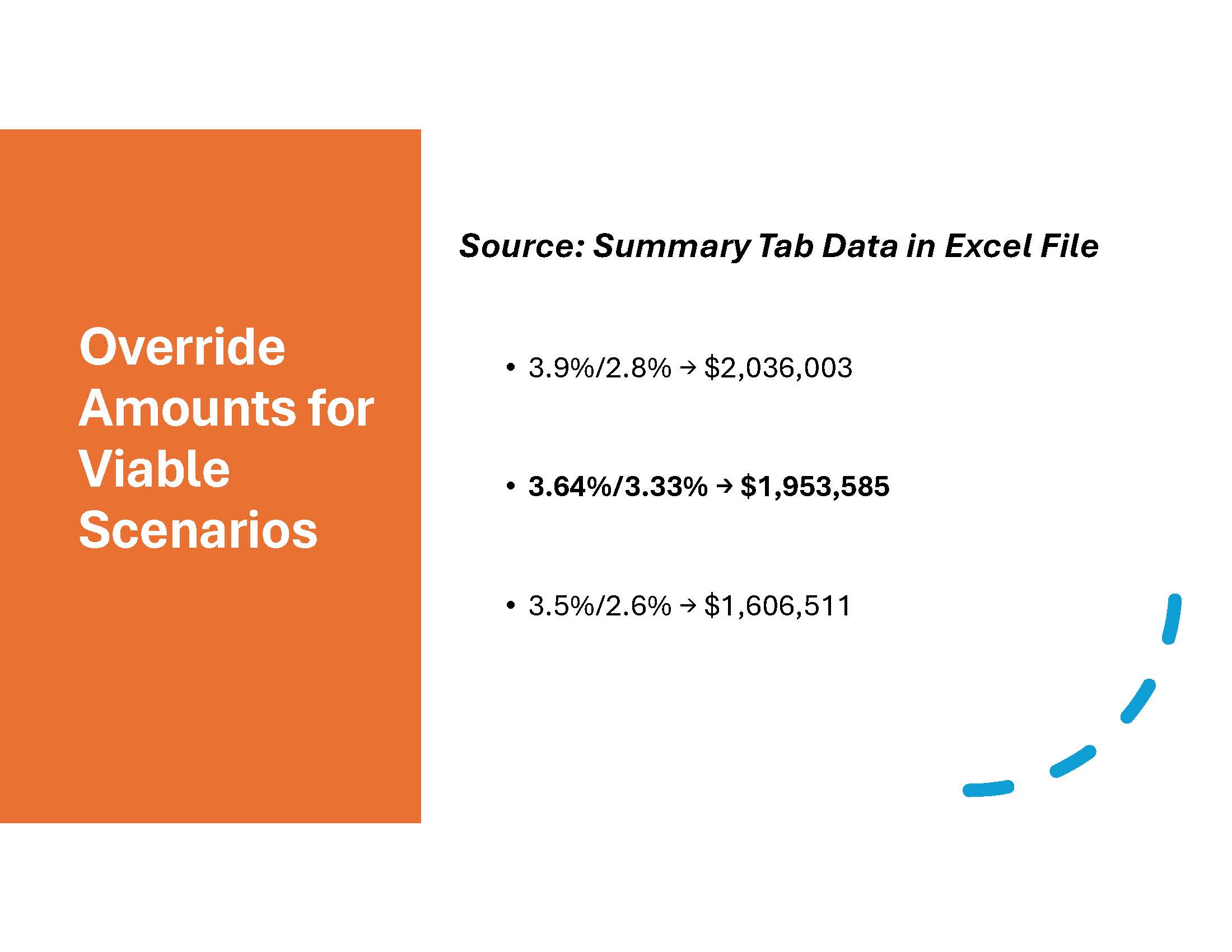

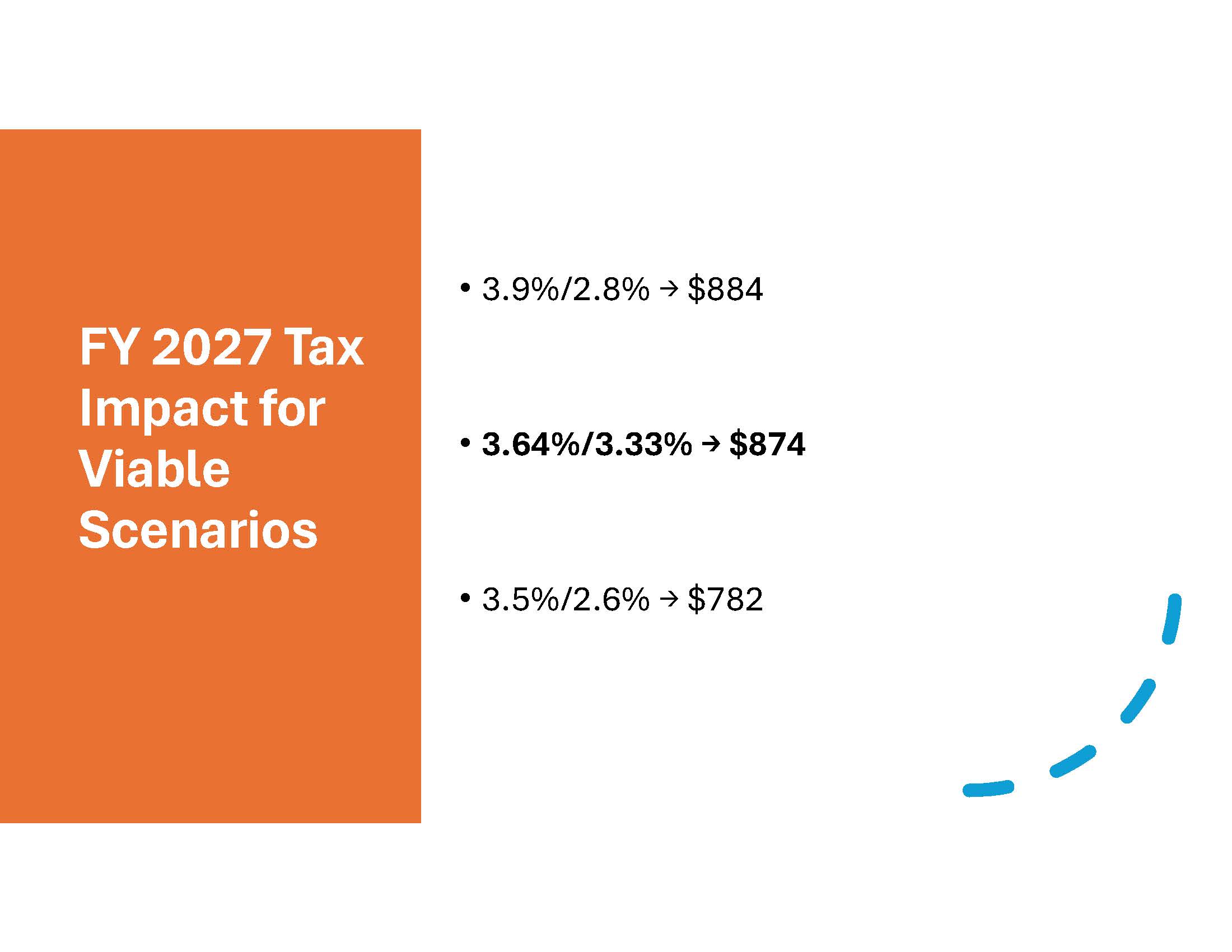

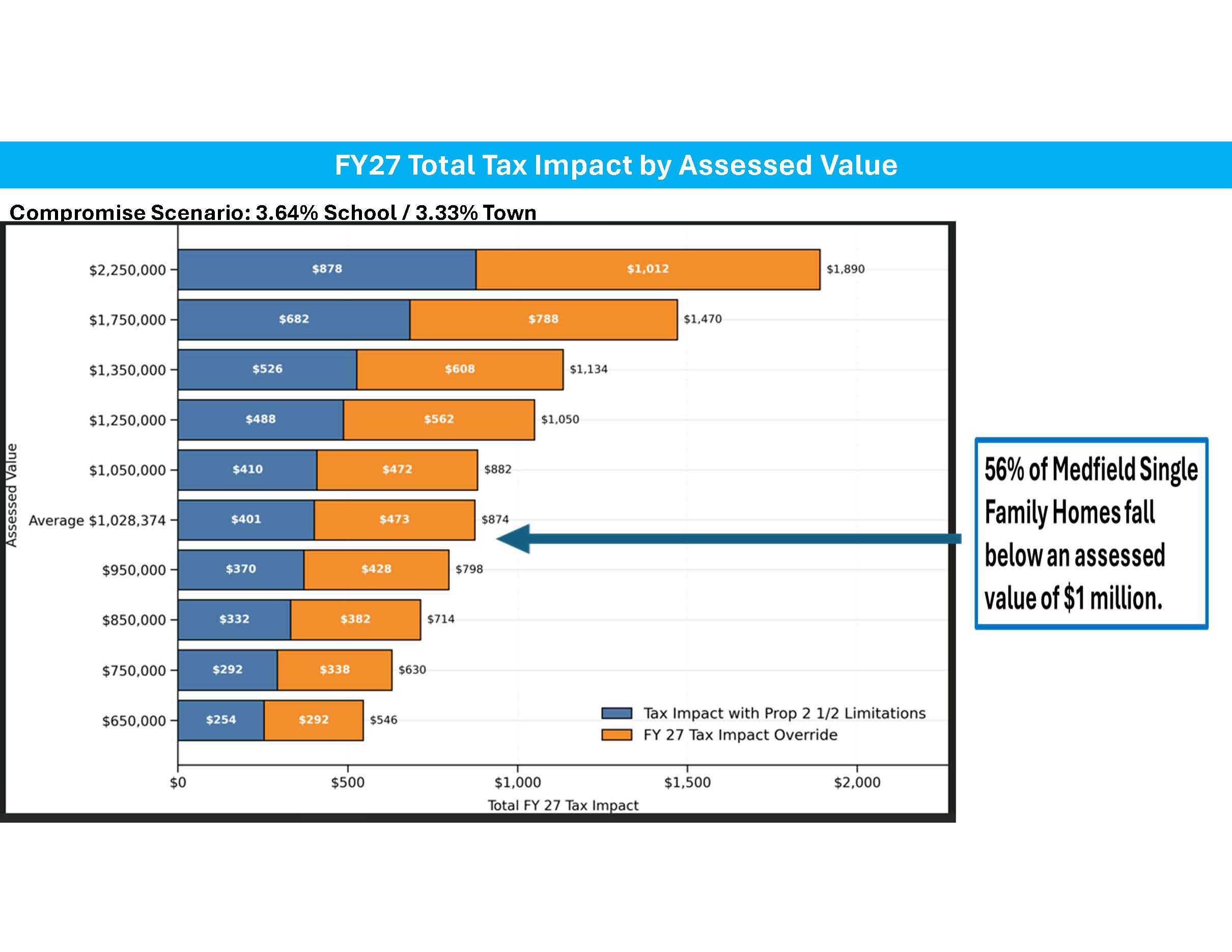

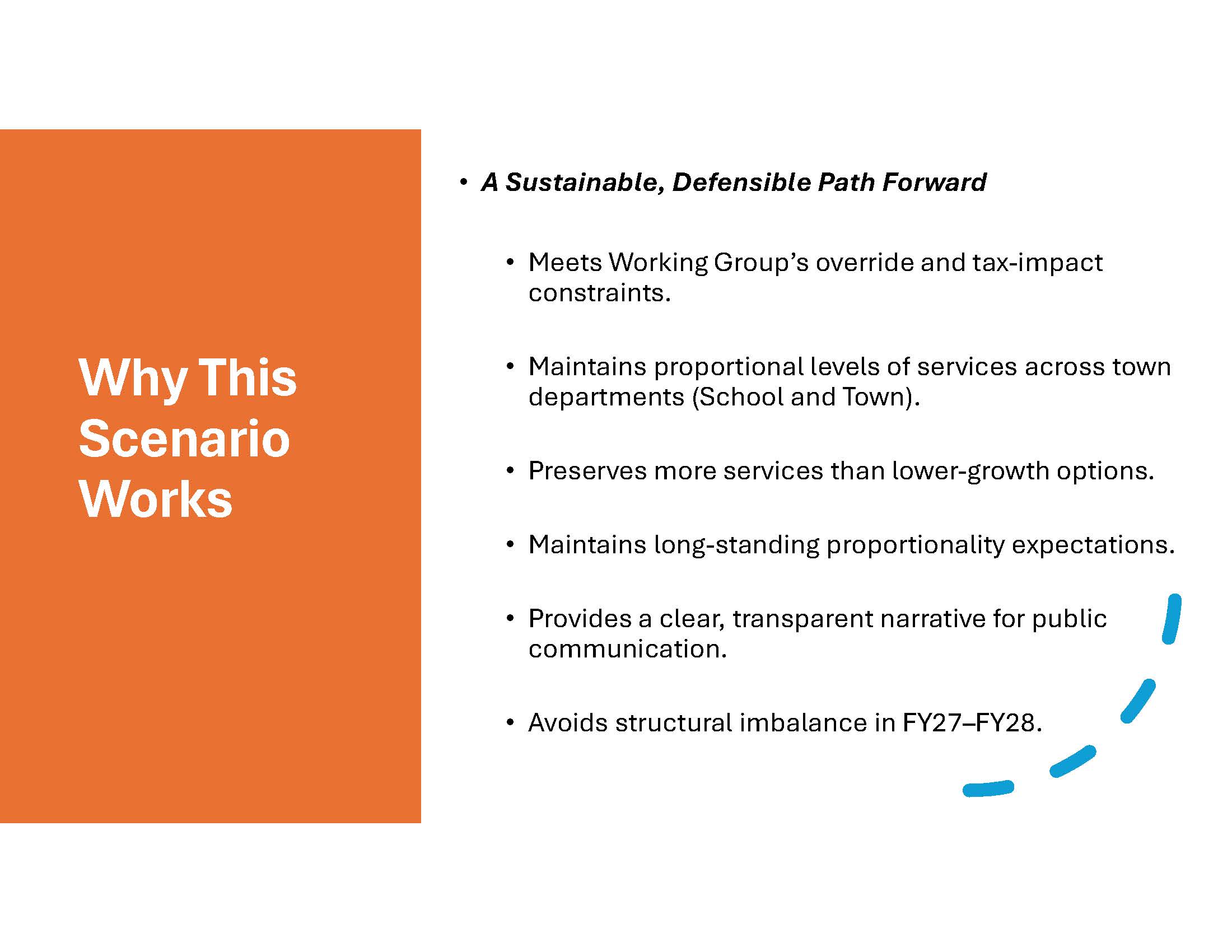

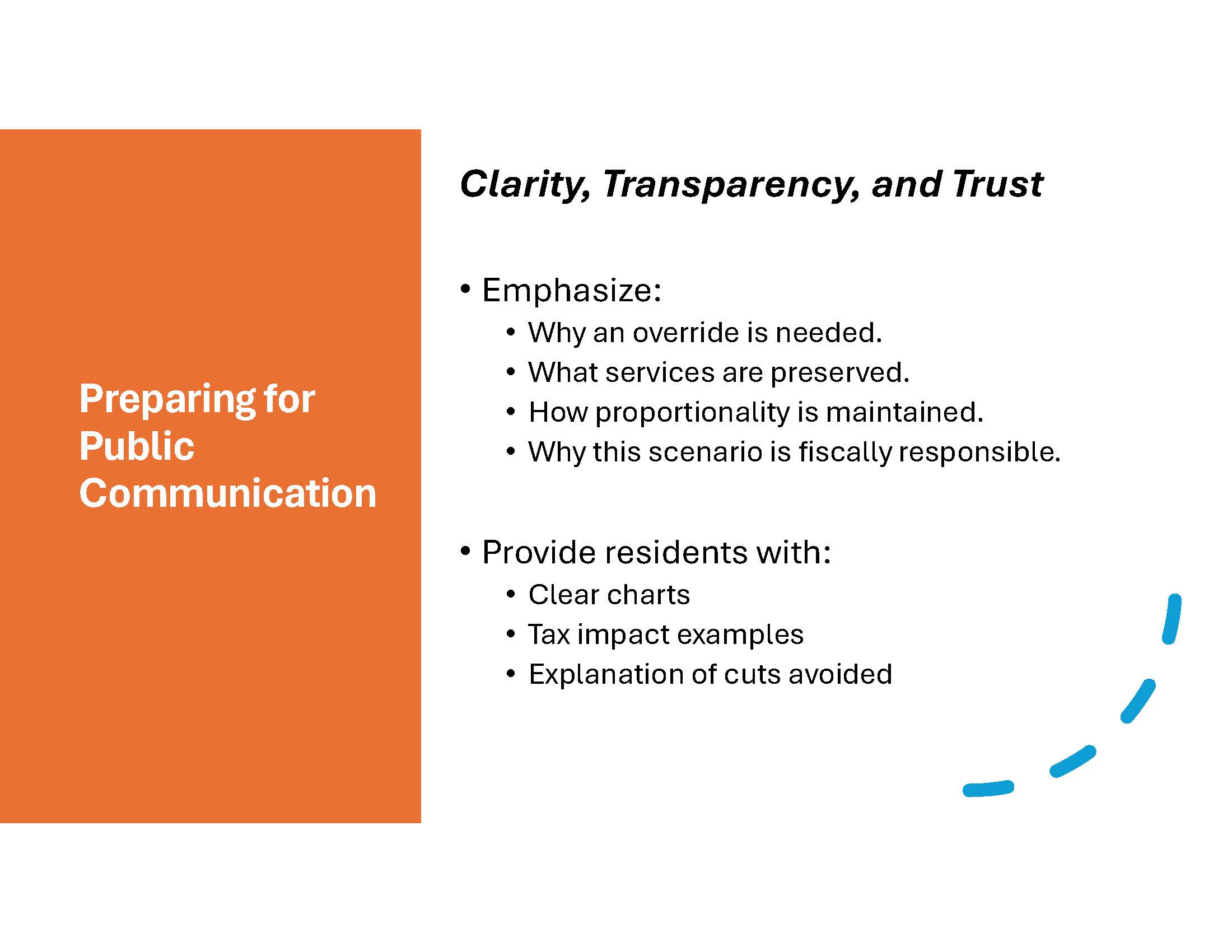

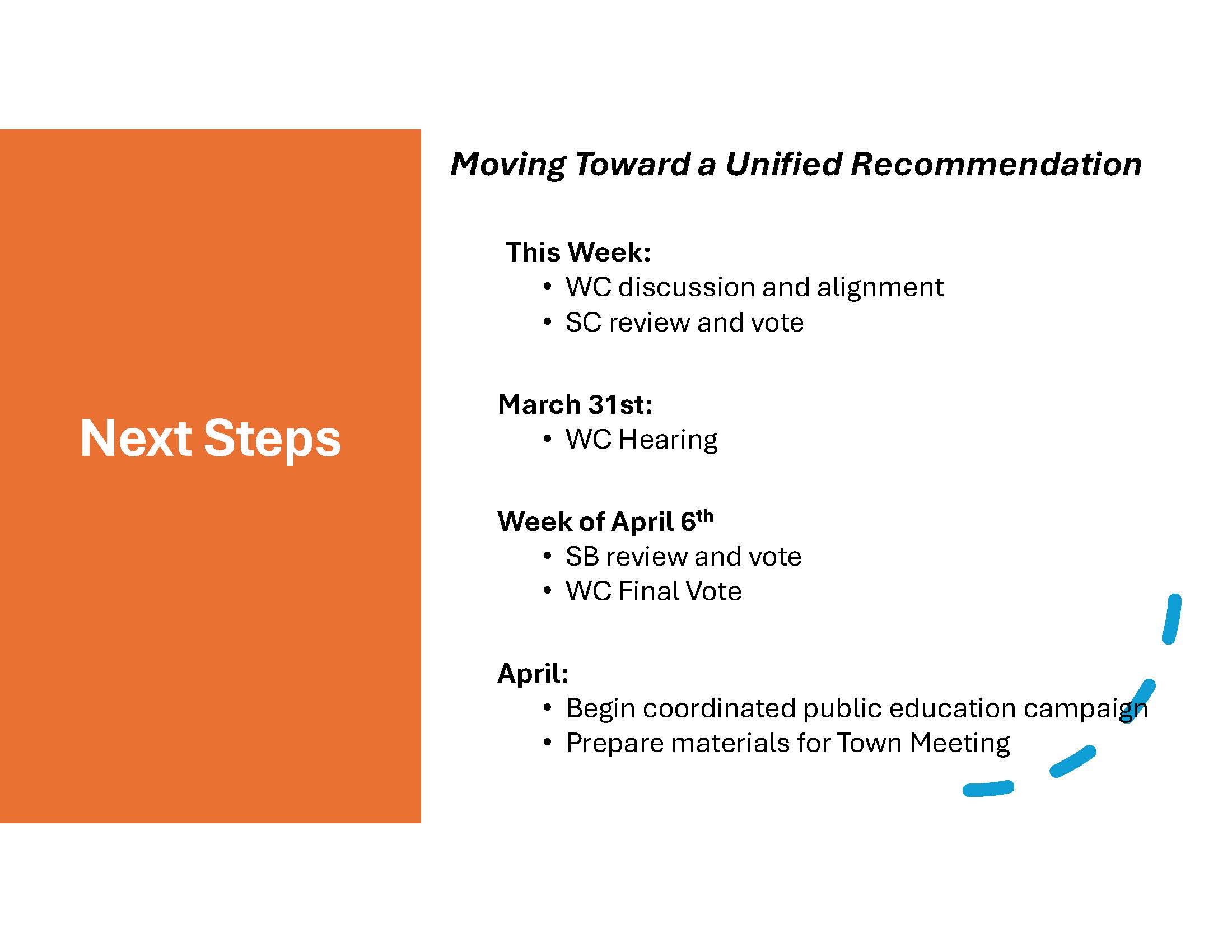

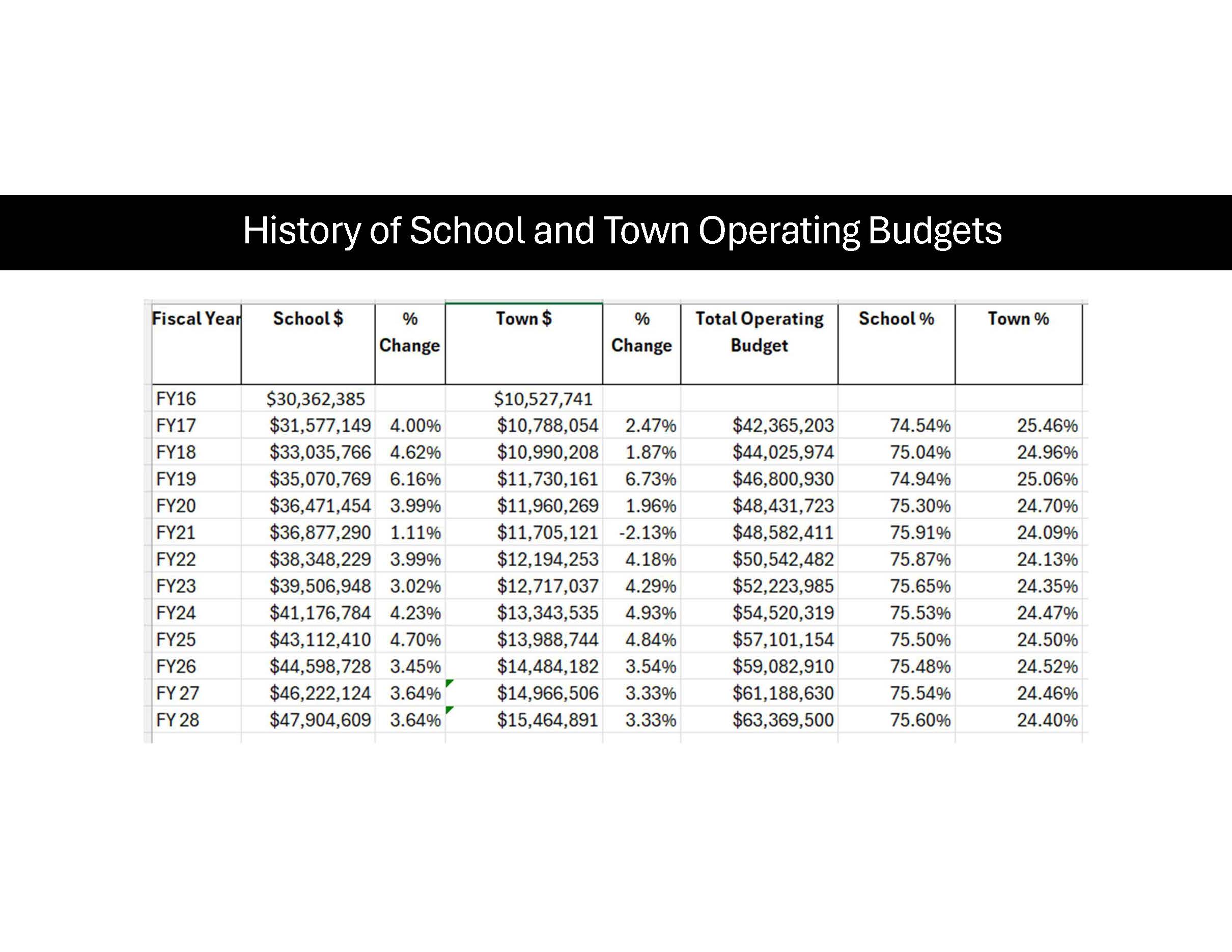

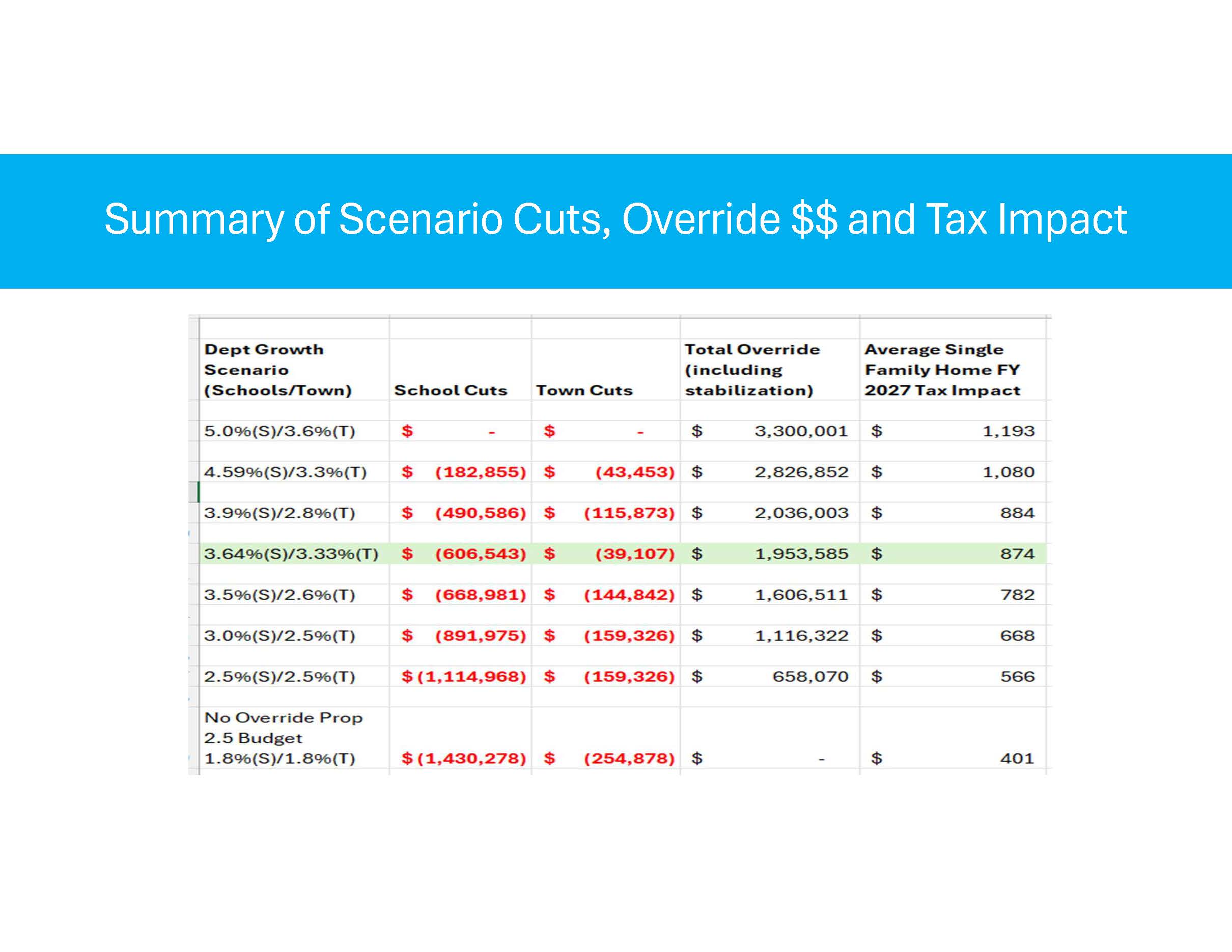

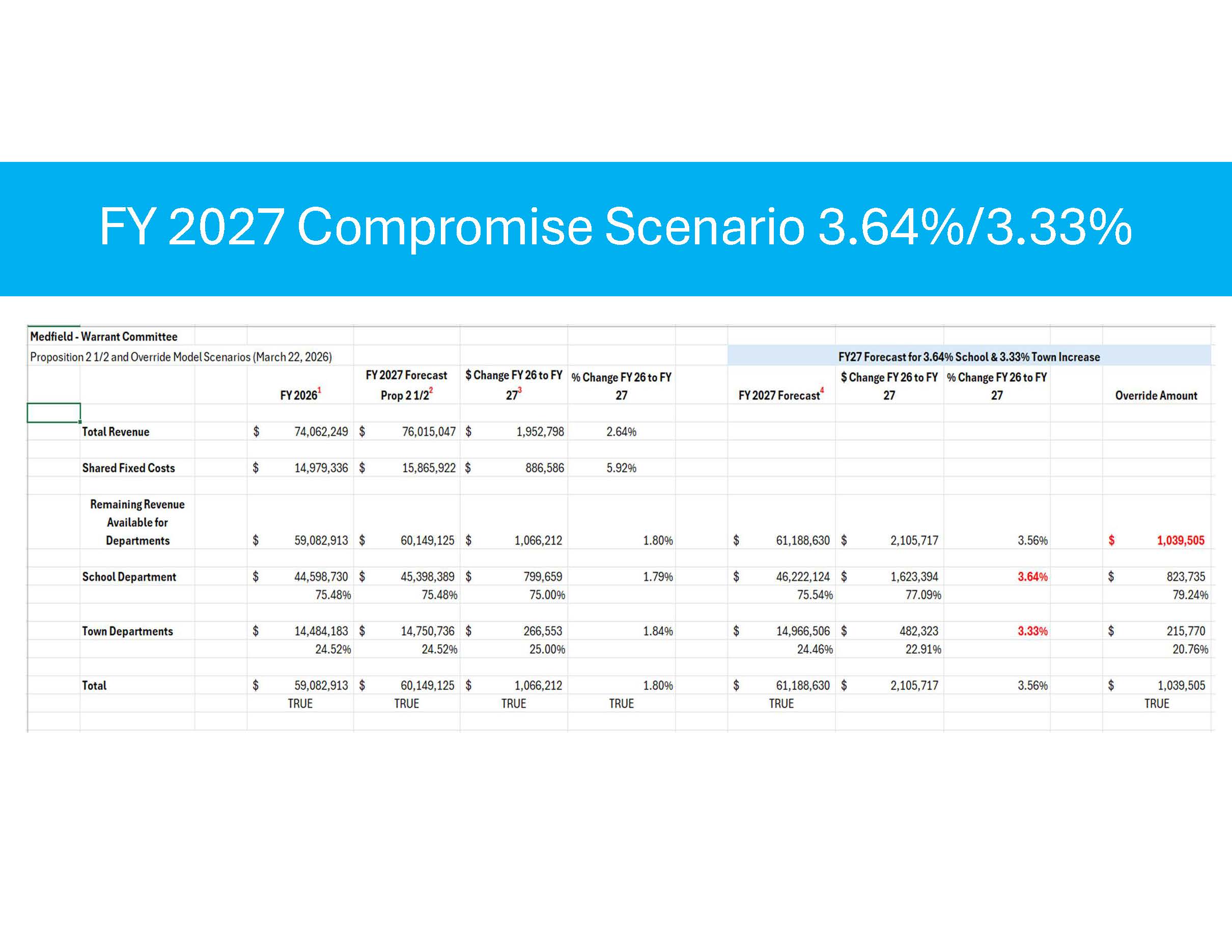

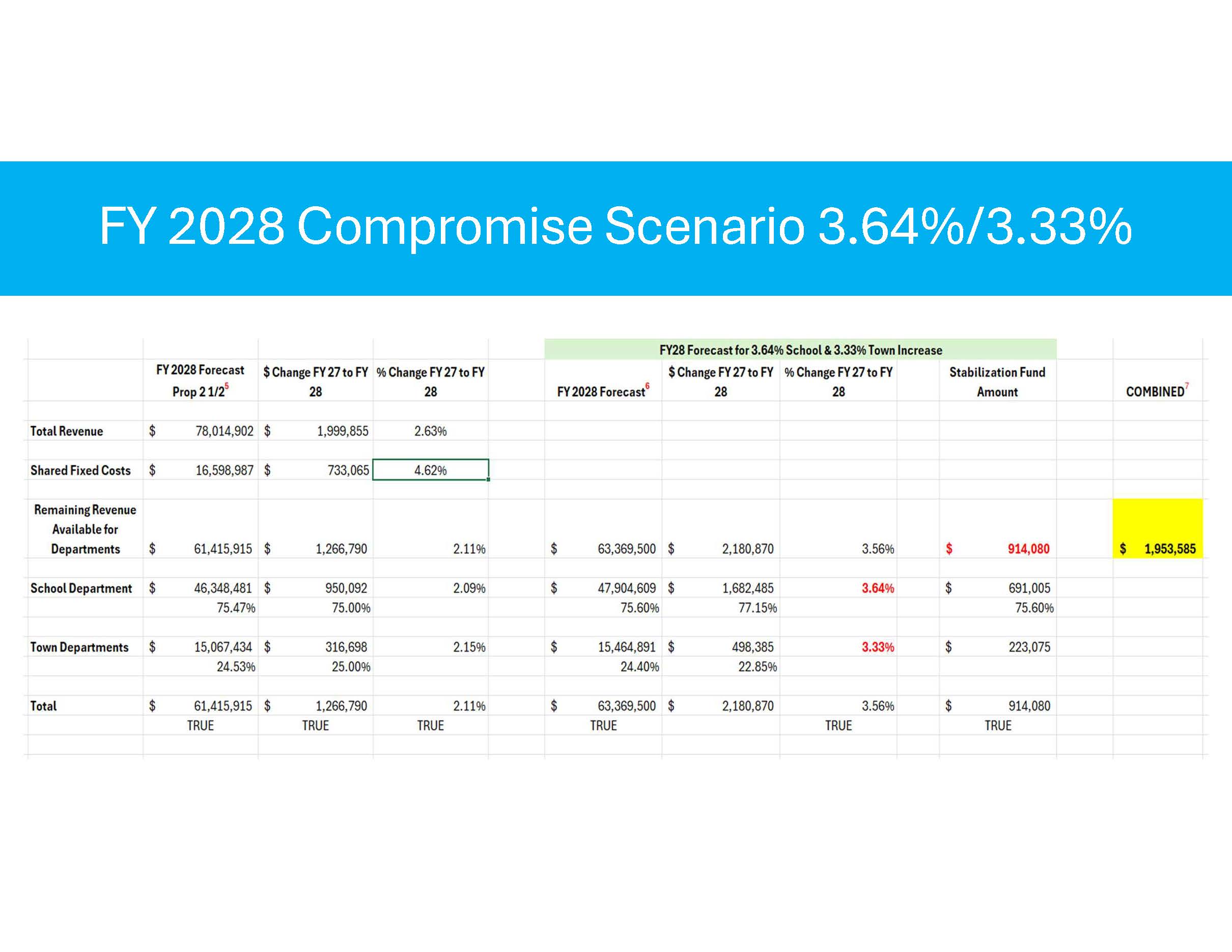

Stephen Callahan, Chair of the Warrant Committee, shared the following slides on how the Warrant Committee reached its decision of the override it is supporting. Steve and the Warrant Committee have been working diligently despite difficult parameters. –

Posted in Financial, Schools, Select Board matters, Town Meeting, Warrant Committee

From DOER –

The Medfield Foundation Legacy Fund has announced that applications are now being accepted for its 2026 Community Impact Grants. Up to $40,000 in grants will be awarded, and any Medfield-based nonprofit or Town department is eligible. Applicants are welcome to submit a grant request online at https://www.medfieldfoundation.org/ by March 15, 2026.

The Medfield Foundation Legacy Fund Community Board will review all submissions and select the finalists who will be invited to PITCH IT!, a Shark Tank-type event to be held in person on April 16, 2026. At PITCH IT!, applicants will present their proposal, goals, and financial needs and directly engage with the Community Board on their projects. The Community Board will make its final selection of grant recipients for the 2026 funding round in late April, 2026.

This year marks the sixth round of Legacy Fund Community Impact grants. To date, over $136,000 has been awarded to thirteen organizations, including the Cultural Alliance of Medfield, the Friends of the MHS Theatre Society, the Friends of the Medfield Rail Trail, Medfield Cares About Prevention, Medfield Outreach, The Peak House Heritage Center, Zullo Gallery and Sustainable Medfield.

Grantees have used their awards to further important projects in Medfield and, in some cases, to leverage significant additional resources such as matching grants or federal or state funding. This year’s applicants should be prepared to illustrate a strong and compelling current need for funds, and possibly present how those funds may generate additional investments in the Medfield community as well.

Act fast to take advantage of this spectacular opportunity!

ABOUT THE MEDFIELD FOUNDATION LEGACY FUND

The Medfield Foundation Legacy Fund is a professionally-managed endowment created to support community-driven projects. Volunteer-run and designed to complement the initiatives of Medfield organizations, the Medfield Foundation Legacy Fund raises private funds for public good. The Legacy Fund invests for the long term while also helping to address current community needs through annual competitive grantmaking for immediate positive impact.

For more information or to contribute to the Medfield Foundation Legacy Fund, please visit https://www.medfieldfoundation.org/.

Make an impact. Leave a Legacy!

The Medfield Foundation Legacy Fund has announced that applications are now being accepted for its 2026 Community Impact Grants. Up to $40,000 in grants will be awarded, and any Medfield-based nonprofit or Town department is eligible. Applicants are welcome to submit a grant request online at https://www.medfieldfoundation.org/ by March 15, 2026.

The Medfield Foundation Legacy Fund Community Board will review all submissions and select the finalists who will be invited to PITCH IT!, a Shark Tank-type event to be held in person on April 16, 2026. At PITCH IT!, applicants will present their proposal, goals, and financial needs and directly engage with the Community Board on their projects. The Community Board will make its final selection of grant recipients for the 2026 funding round in late April, 2026.

This year marks the sixth round of Legacy Fund Community Impact grants. To date, over $136,000 has been awarded to thirteen organizations, including the Cultural Alliance of Medfield, the Friends of the MHS Theatre Society, the Friends of the Medfield Rail Trail, Medfield Cares About Prevention, Medfield Outreach, The Peak House Heritage Center, Zullo Gallery and Sustainable Medfield.

Grantees have used their awards to further important projects in Medfield and, in some cases, to leverage significant additional resources such as matching grants or federal or state funding. This year’s applicants should be prepared to illustrate a strong and compelling current need for funds, and possibly present how those funds may generate additional investments in the Medfield community as well.

Act fast to take advantage of this spectacular opportunity!

ABOUT THE MEDFIELD FOUNDATION LEGACY FUND

The Medfield Foundation Legacy Fund is a professionally-managed endowment created to support community-driven projects. Volunteer-run and designed to complement the initiatives of Medfield organizations, the Medfield Foundation Legacy Fund raises private funds for public good. The Legacy Fund invests for the long term while also helping to address current community needs through annual competitive grantmaking for immediate positive impact.

For more information or to contribute to the Medfield Foundation Legacy Fund, please visit https://www.medfieldfoundation.org/.

Make an impact. Leave a Legacy!

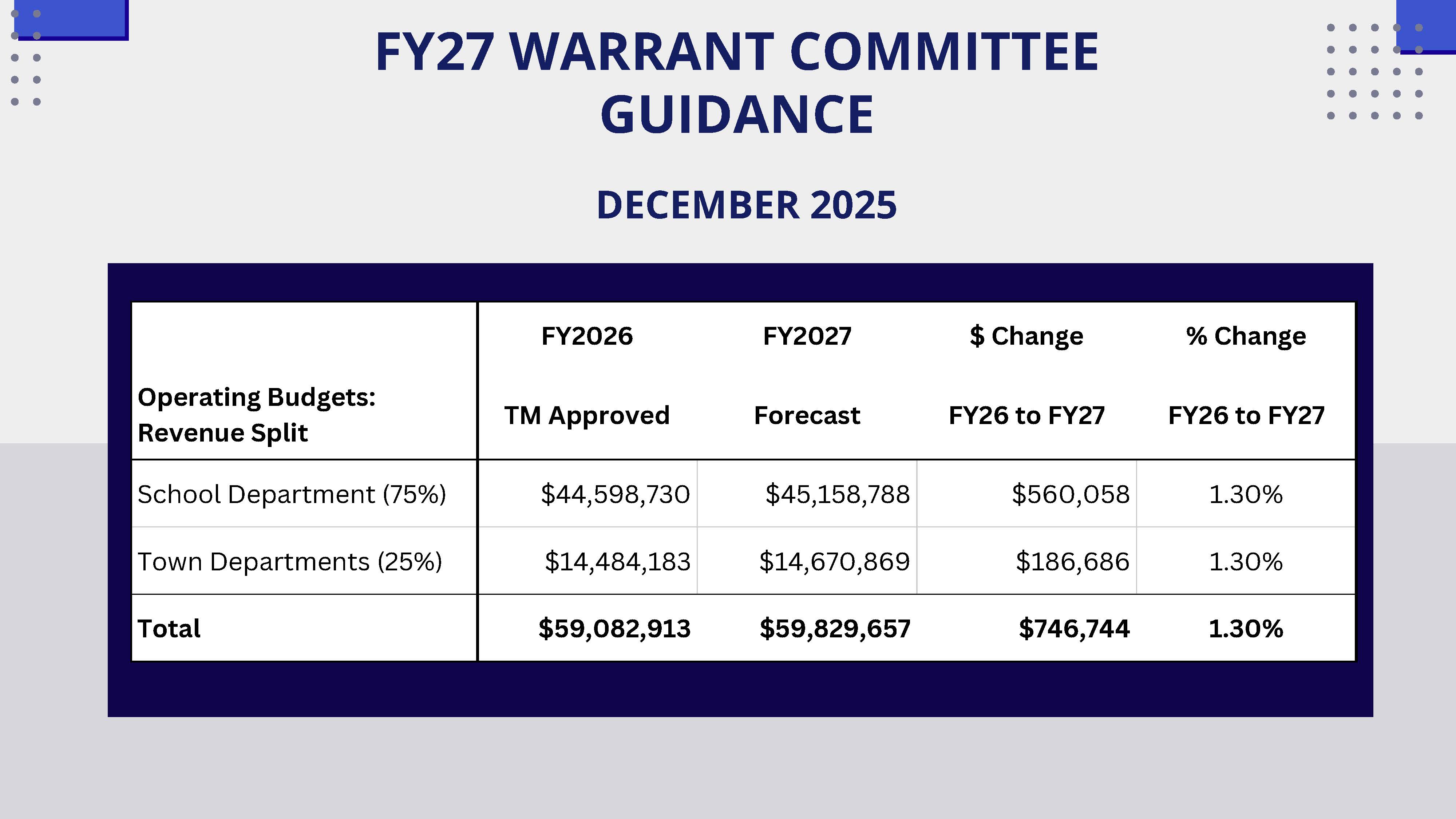

From Stephen Callahan, Chair of the Warrant Committee, this afternoon –

Comments Off on Warrant Committee on Budget/Override

Posted in Budgets, Financial, Town Meeting, Town Services, Warrant Committee

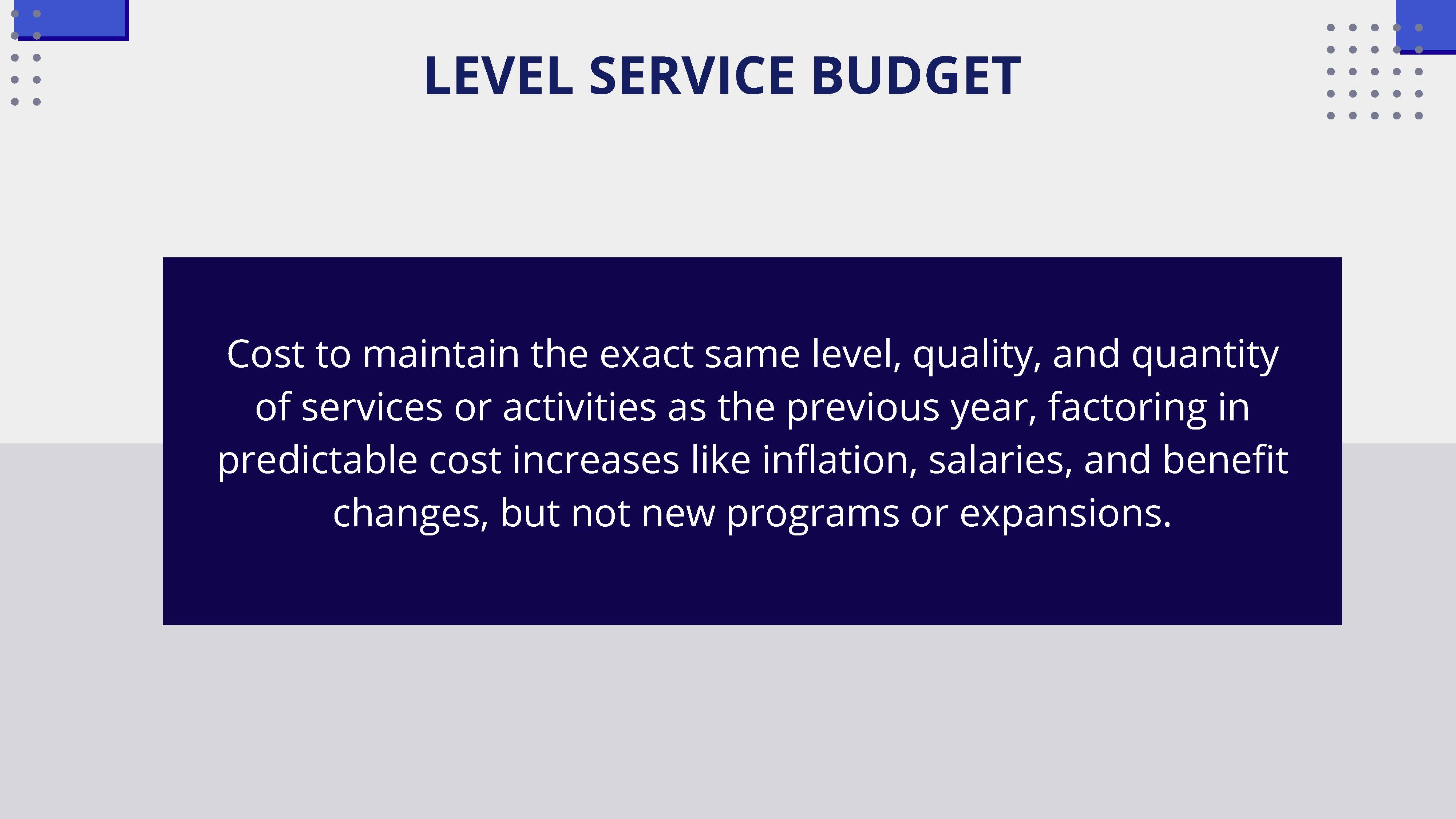

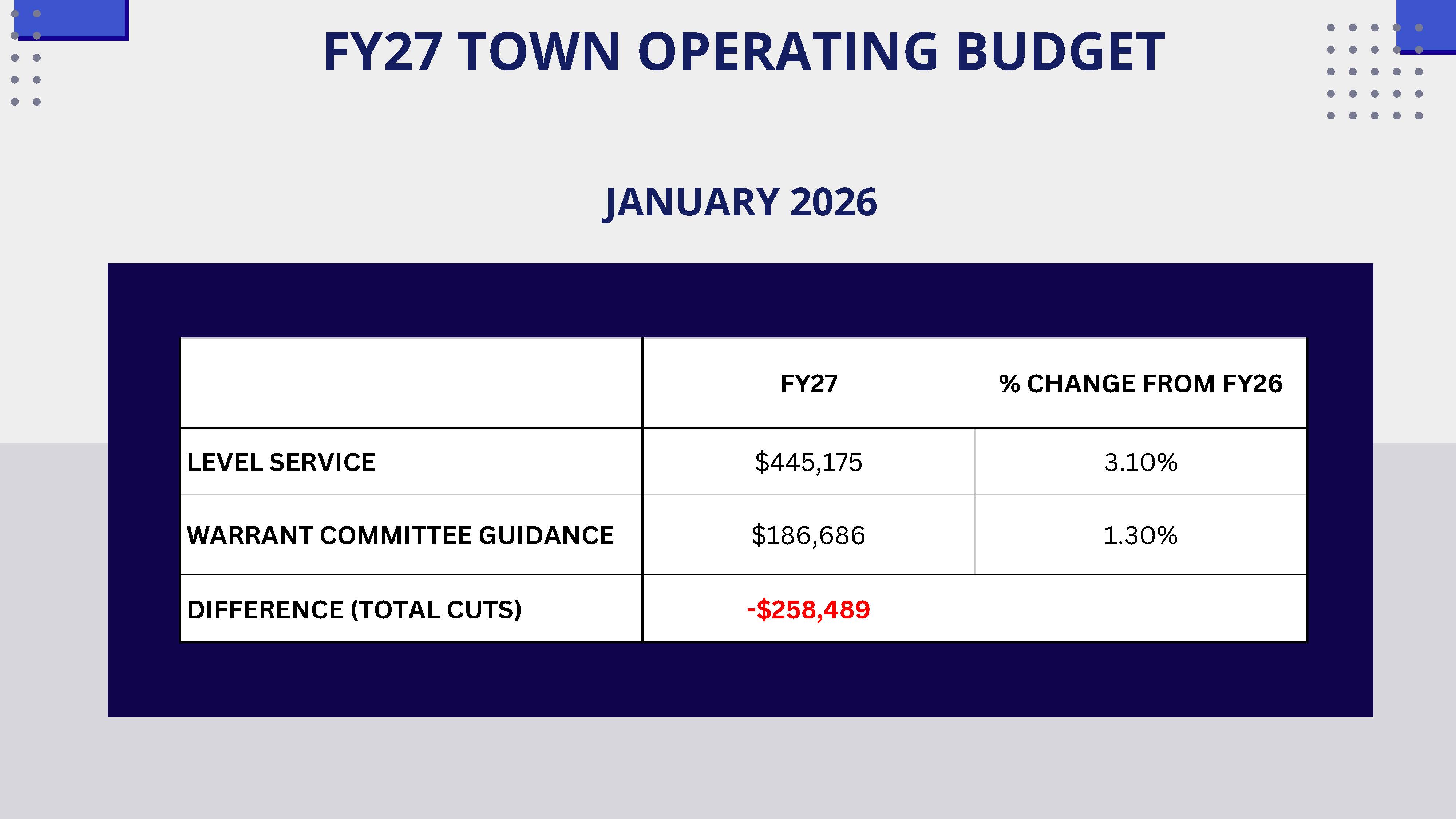

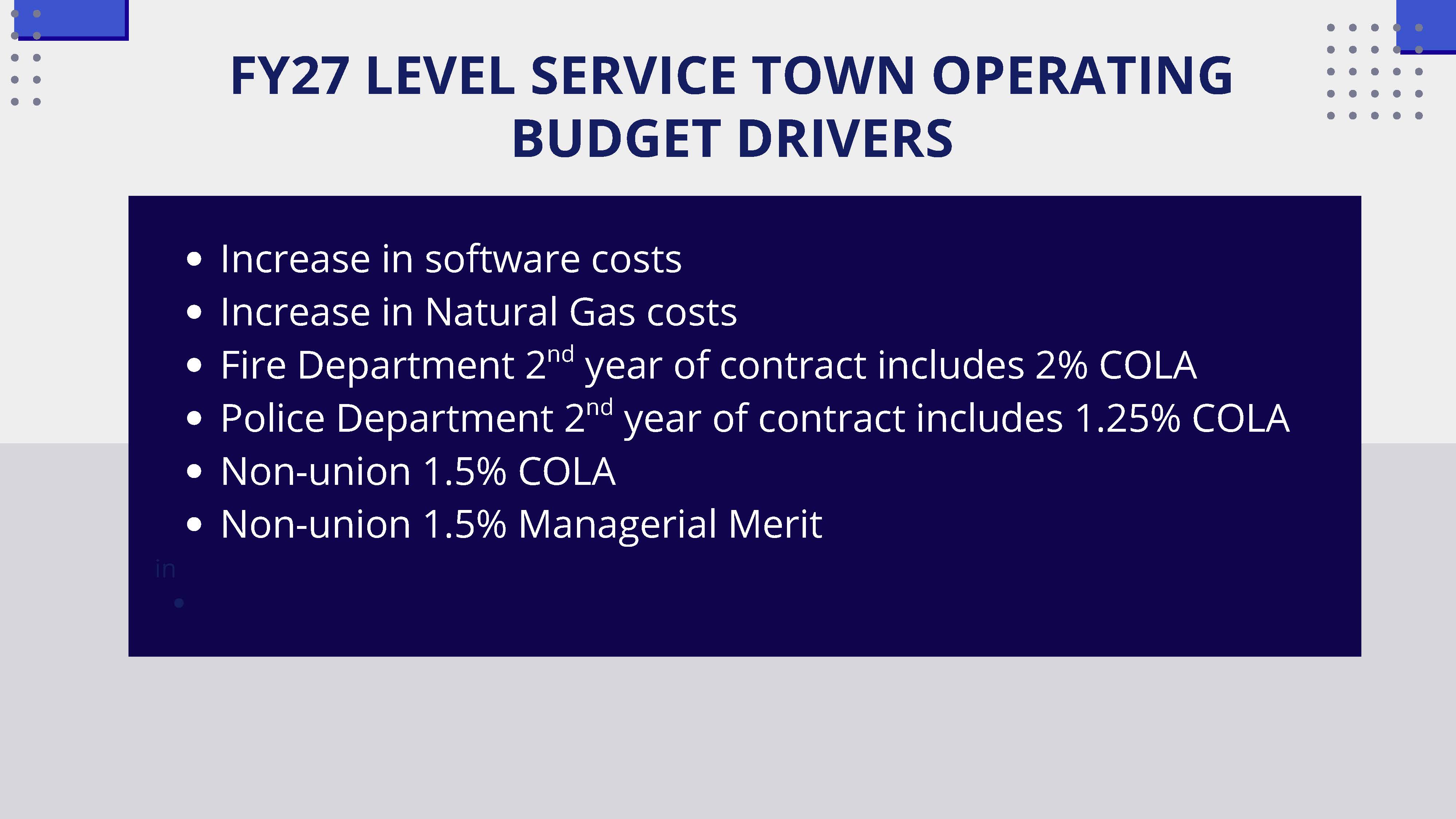

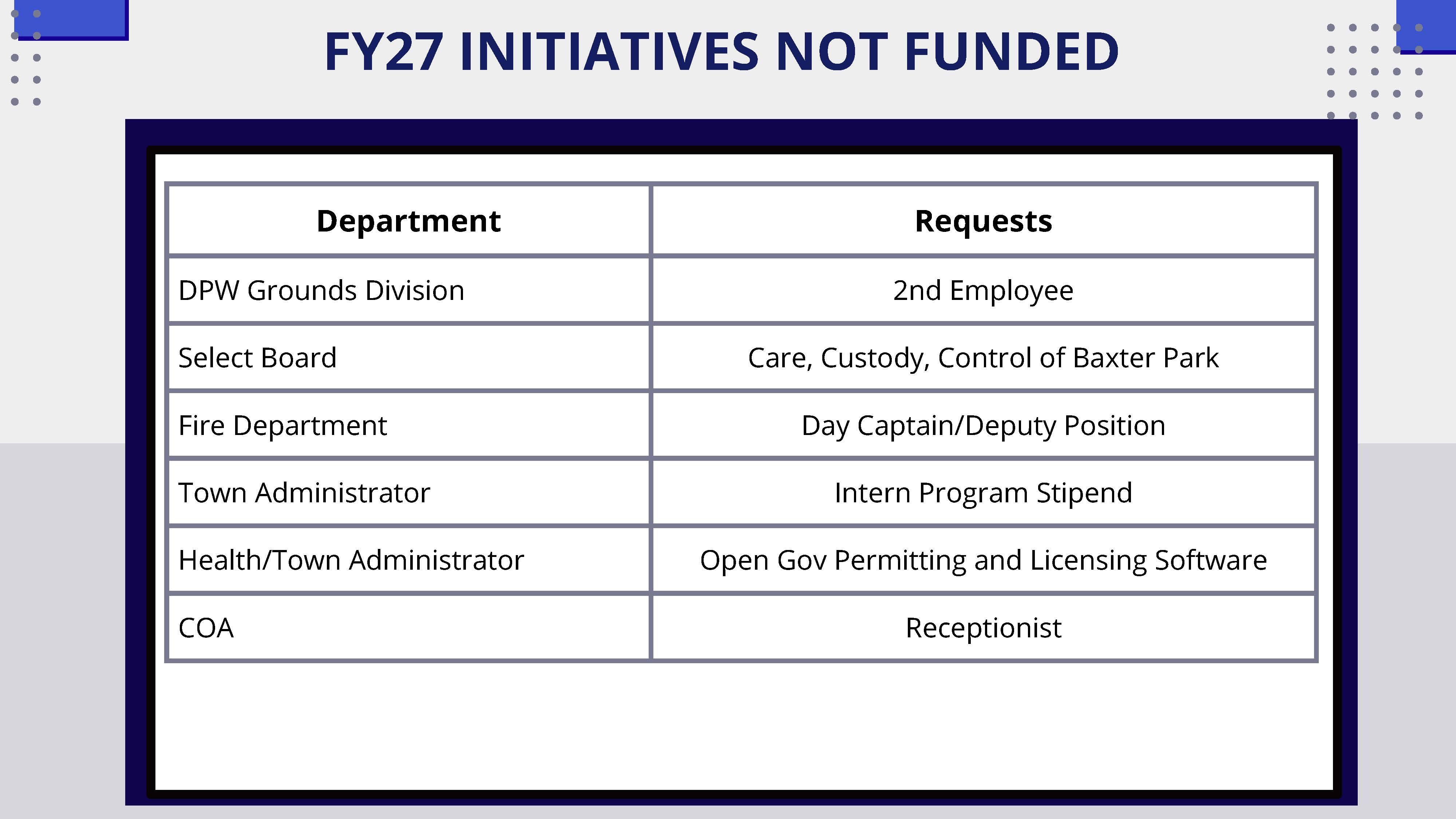

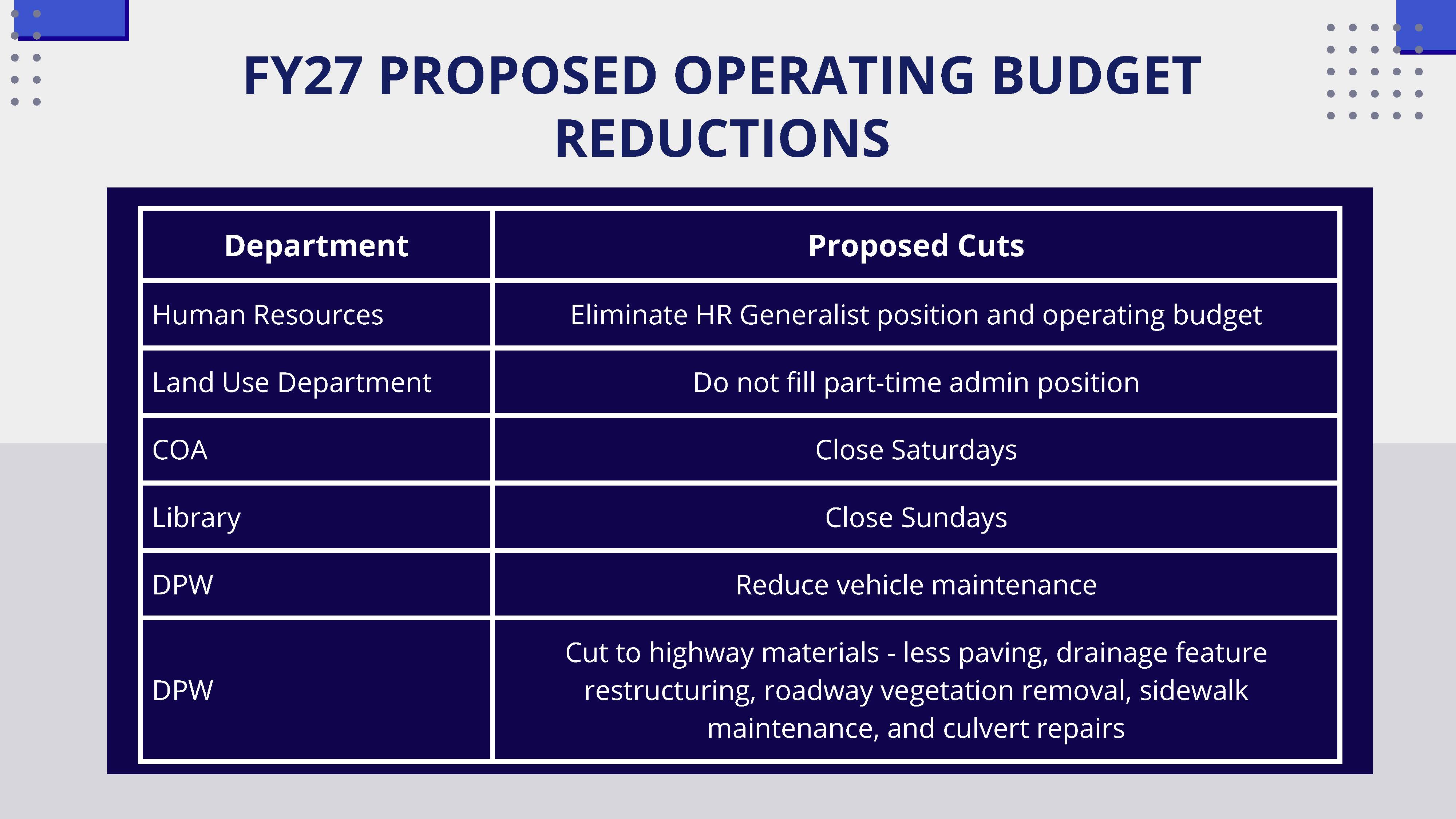

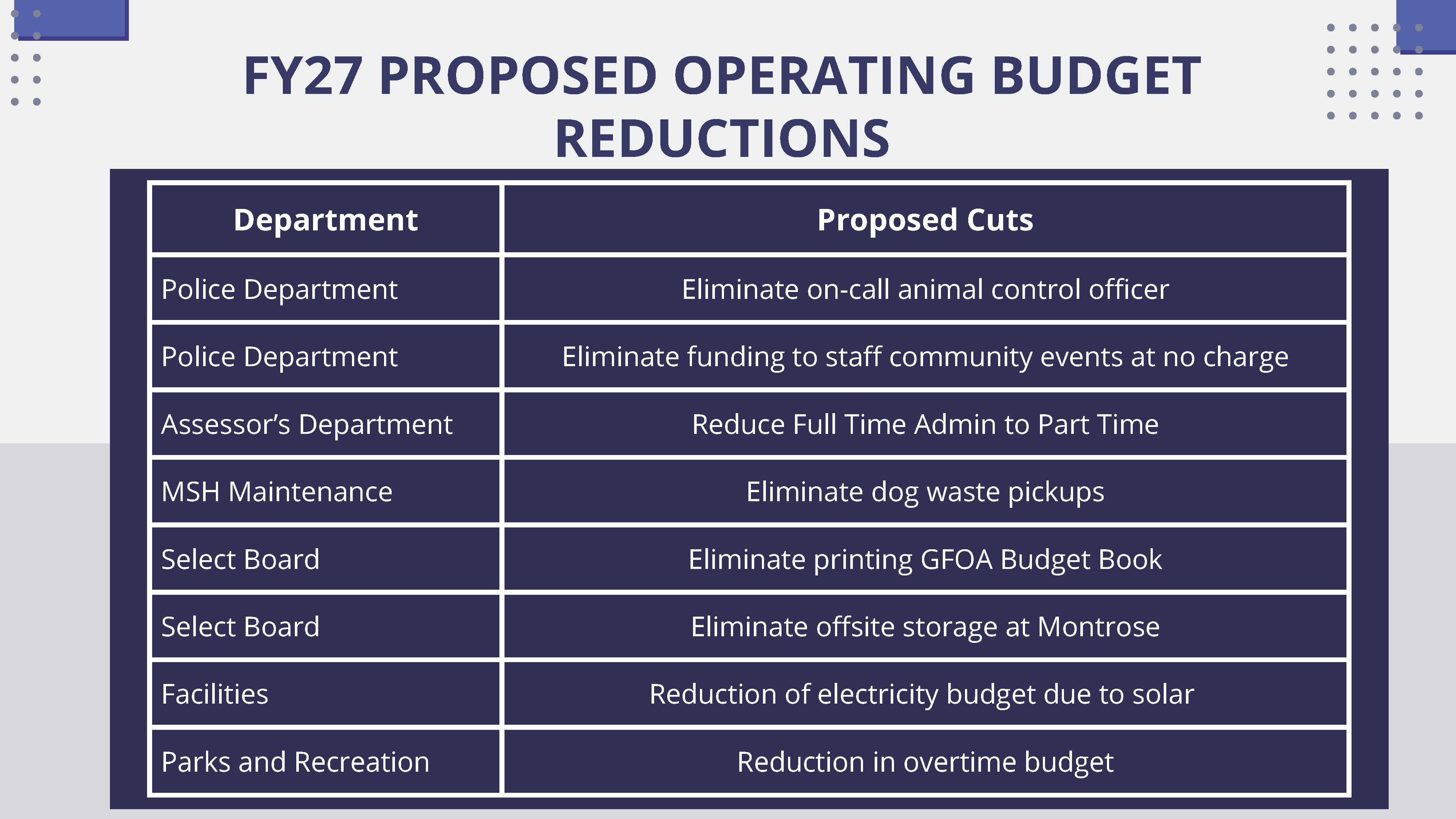

From Town Administrator, Kristine Trierweiler this morning, her FY27 PROPOSED OPERATING BUDGET

REDUCTIONS to the Warrant Committee last night –

Comments Off on FY27 PROPOSED OPERATING BUDGET REDUCTIONS

Posted in Budgets, Financial, Town Meeting, Town Services

Medfield Select Board member

I started this blog to share the interesting and useful information that I saw while doing my job as a Medfield select board member. I thought that my fellow Medfield residents would also find that information interesting and useful as well. This blog is my effort to assist in creating a system to push the information out from the Town House to residents. Let me know if you have any thoughts on how it can be done better.

For information on my other job as an attorney (personal injury, civil litigation, estate planning and administration, and real estate), please feel free to contact me at 617-969-1500 or Osler.Peterson@OslerPeterson.com.

| Amy Cohen on Delineator Flexposts – t… | |

| Zach on Warrant Committee’s slid… | |

| Donna Knott on Reading for “Read Across… | |

| Lester Cohen on Town’s Buildings Require… | |

| Select Board member… on Black Out at Budget Works… |