From:

- Richard DeSorgher (first),

- Norfolk Registrar of Deeds (second – Medfield paid in $166,440.00), and

- the Division of Local Services (DLS) newsletter this week –

===============================================

From: Richard DeSorgher

Sent: Monday, February 1, 2021 5:03 PM

To: Osler Peterson

Subject: Community Preservation Funds

Hi Pete,

Hope you are well and staying safe during this most trying of times, especially as a town selectmen. I know you and I talked about the importance and common sense tax-saving ability adopting the Community Preservation Act would be for Medfield, so I am attaching the notice sent to me from the Registry of Deeds about the land document surcharges Medfield has forwarded to the Community Preservation fund; that sadly Medfield is missing out on but of which 186 other communities are taking advantage.

I was appointed to the Historical Committee down here in Mashpee and I have seen the advantage of those funds. Mashpee originally contributed 3% to the CPC funds. We have since reduced it by one percent, having a one percent surcharge instead go towards waste-water treatment in the town.

We have approved through the Community Preservation funds a new war memorial for the town veterans, a community garden, a playground, a dog park, a pickleball court (a sport I had never heard of before moving here),funding for low-income housing, money to preserve the Mashpee Parsonage, one of the oldest structures in town, preserving early town records, purchasing conservation land (a former bog), just to name a few in the short time I have been down here.

It is such an important and money saving act that the town has adapted.

Towns, like Medfield, are contributing to the system but are not receiving any of the benefits and instead must fund town projects at 100% instead of having the CPC funds to help lessen the taxpayers’ load.

I know I am preaching to the choir but just wanted to send along the Registry of Deeds letter in case you did not receive one and to give some re-enforcing support now that I have actually seen it in action.

Stay well and thanks for all you and the town government does for the citizens of Medfield.

Richard

![WILLIAM P. O 'DONNELL

REGISTER OF DEEDS

ASSISTANT RECORDER OF THE

LAND COURT

Selectman Osler L. Peterson

Medfield Board of Selectmen

10 Copperwood Road

Medfield, MA 02052

Dear Selectman Peterson,

COUNTY OF NORFOLK

COUNTY O F PRESIDENTS

REGISTRY OF DEEDS

NORFOLK REGISTRY DISTRICT OF THE LAND COURT

January 20, 2021

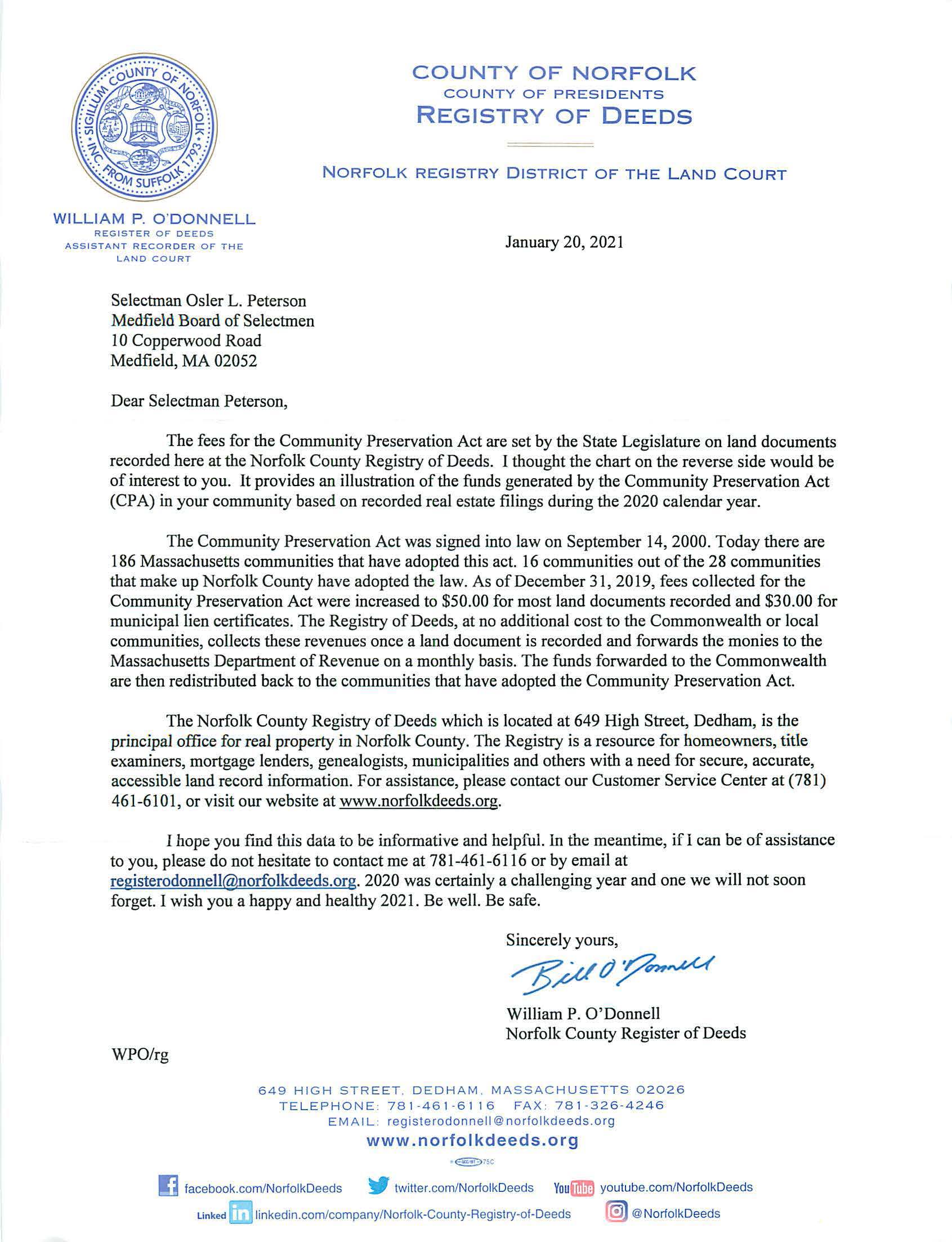

The fees for the Community Preservation Act are set by the State Legislature on land documents

recorded here at the Norfolk County Registry of Deeds. I thought the chart on the reverse side would be

of interest to you. It provides an illustration of the funds generated by the Community Preservation Act

(CPA) in your community based on recorded real estate filings during the 2020 calendar year.

The Community Preservation Act was signed into law on September 14, 2000. Today there are

186 Massachusetts communities that have adopted this act. 16 communities out of the 28 communities

that make up Norfolk County have adopted the law. As of December 31, 2019, fees collected for the

Community Preservation Act were increased to $50.00 for most land documents recorded and $30.00 for

municipal lien certificates. The Registry of Deeds, at no additional cost to the Commonwealth or local

communities, collects these revenues once a land document is recorded and forwards the monies to the

Massachusetts Department of Revenue on a monthly basis. The funds forwarded to the Commonwealth

are then redistributed back to the communities that have adopted the Community Preservation Act.

The Norfolk County Registry of Deeds which is located at 649 High Street, Dedham, is the

principal office for real property in Norfolk County. The Registry is a resource for homeowners, title

examiners, mortgage lenders, genealogists, municipalities and others with a need for secure, accurate,

accessible land record information. For assistance, please contact our Customer Service Center at (781)

461-6101 , or visit our website at www .norfolkdeeds.org.

1 hope you find this data to be informative and helpful. In the meantime, if I can be of assistance

to you, please do not hesitate to contact me at 781-461-6116 or by email at

registerodonnell@norfolkdeeds.org. 2020 was certainly a challenging year and one we will not soon

forget. I wish you a happy and healthy 2021. Be well. Be safe.

WPO/rg

Sincerely yours,

~//frJP~

William P. O'Donnell

Norfolk County Register of Deeds

649 HIGH STREET. DEDHAM . MASSACHUSETTS 02026

TE L EPHONE : 781 -461-6 11 6 FAX : 781-326-4246

EM Al L : registerodonnell@norfolkdeeds.org

www.norfolkdeeds.org

I] facebook.com/NorfolkDeeds ~ twitter.com/NorfolkDeeds You(g youtube.com/NorfolkDeeds

linked fm linkedin.com/company/Norfolk-County-Registry-of-Deeds ~ @NorfolkDeeds

NORFOLK COUNTY REGISTRY OF DEEDS

COMMUNITY PRESERVATION ACT (CPA)

SURCHARGES BY TOWN FOR CALENDAR YEAR 2020

TOWN TOTAL

AVON $60,260.00

BELLINGHAM $219,660.00

BRAINTREE $400,235.00

BROOKLINE $478,050.00

CANTON $269,455.00

COHASSET $147,775.00

DEDHAM $288,320.00

DOVER $86,525.00

FOXBOROUGH $199,605.00

FRANKLIN $393,210.00

HOLBROOK $125,170.00

MEDFIELD $166,440.00

MEDWAY $158,550.00

MIUJS $117,615.00

MILTON $329,310.00

NEEDHAM $389,610.00

NORFOLK $155,295.00

NORWOOD $266,565.00

PIAINVILLE $102,095.00

QUINCY $731,850.00

RANDOLPH $279,160.00

SHARON $230,840.00

STOUGHTON $288,795.00

WALPOLE $314,670.00

WELLESLEY $312,495.00

WESTWOOD $189,110.00

WEYMOUTH $620,970.00

WRENTHAM $171,120.00](https://medfield02052.blog/wp-content/uploads/2021/02/20210120-norfolk-registry-of-deeds-ltr-from_page_2.jpg)

===============================================

Ask DLS: Community Preservation Act – Part 8

This month’s Ask DLS features Part 8 of frequently asked questions concerning the Community Preservation Act (CPA) and CPA funding for eligible open space projects. Additional questions about the CPA will be featured in future editions of City & Town. For Part 7 of the series, see the January 7, 2021 edition of City & Town. For additional information on the Community Preservation Act see Informational Guideline Release (IGR) 19-14. Please let us know if you have other areas of interest or send a question to cityandtown@dor.state.ma.us. We would like to hear from you.

In general, what community preservation projects are eligible for funding under the CPA?

There are three community preservation project or asset categories: (1) open space (including land for recreational use); (2) historic resources; and (3) community housing. These FAQs will discuss CPA funding for projects relating to open space.

What is the definition of “open space?”

“Open space” is defined in G.L. c. 44B, § 2 to “include, but not be limited to, land to protect existing and future well fields, aquifers and recharge areas, watershed land, agricultural land, grasslands, fields, forest land, fresh and salt water marshes and other wetlands, ocean, river, stream, lake and pond frontage, beaches, dunes and other coastal lands, lands to protect scenic vistas, land for wildlife or nature preserve and land for recreational use.”

For what purposes may CPA funds be spent regarding open space?

The CPA clarifies allowable community preservation project expenditures through its definitions which are found in G.L. c. 44B, § 2. As a result, the CPA definitions should always be reviewed when determining if an expenditure is allowable.

Acquisition, creation, and preservation – CPA funds may be spent for the acquisition, creation, and preservation of open space.

“Acquisition” is defined in G.L. c. 44B, § 2 as “obtain[ing] by gift, purchase, devise, grant, rental, rental purchase, lease or otherwise.” ”Acquire” does not include a taking by eminent domain, except as provided under c. 44B.

“Creation” – There is not a specific definition of “creation” under the CPA; however, “creation” was defined by the court for CPA purposes in the case of Seideman v. City of Newton, 452 Mass. 472 (2008) to mean “to bring into being or to cause to exist.”

“Preservation” is defined under G.L. c. 44B, § 2 as “protection of personal or real property from injury, harm or destruction.”

Rehabilitation or restoration of open space – CPA funds may also be spent for the rehabilitation or restoration of open space; provided the open space was acquired or created with community preservation funds.

”Rehabilitation” is defined under G.L. c. 44B, § 2 as “capital improvements, or the making of extraordinary repairs, to historic resources, open spaces, lands for recreational use and community housing for the purpose of making such historic resources, open spaces, lands for recreational use and community housing functional for their intended uses including, but not limited to, improvements to comply with the Americans with Disabilities Act and other federal, state or local building or access codes; provided, that with respect to historic resources, ”rehabilitation” shall comply with the Standards for Rehabilitation stated in the United States Secretary of the Interior’s Standards for the Treatment of Historic Properties codified in 36 C.P.R. Part 68; and provided further, that with respect to land for recreational use, ”rehabilitation” shall include the replacement of playground equipment and other capital improvements to the land or the facilities thereon which make the land or the related facilities more functional for the intended recreational use.

“Restoration” is not defined under the CPA and we are not aware of any cases defining “restoration” in the CPA context. In the absence of such an interpretation, we look to the usual and generally understood meaning of words from sources known to the legislature, such as use in other legal contexts and dictionary definitions. See Seideman v. Newton, 452 Mass. 472, 477-478 (2008). At webster-dictionary.org, “restoration” is defined as “the act of restoring or bringing back to a former place, station, or condition.”

What are some examples of allowable CPA open space projects?

Acquisition of open space – Acquisition of real property or an interest in real property is allowable for open space purposes, including the acquisition of agricultural land, grasslands, fields, forest land, watershed land, fresh and salt water marshes and other wetlands, ocean, river, stream, lake and pond frontage, beaches, dunes and other coastal lands, land to protect scenic vistas, land for wildlife or a nature preserve, land for recreational use and land to protect existing and future well fields, aquifers and recharge areas. Again, one must look to G.L. c. 44B, § 2, to determine the definitions of “real property” and “real property interest” for CPA expenditure purposes. Under G.L. c. 44B, § 5(f), the price of an acquisition must not exceed the value of the property as determined through “procedures customarily accepted by the appraising profession as valid.” And, under G.L. c. 44B, § 12, real property interests financed in whole or in part with CP Fund monies must be bound by a permanent restriction which conforms to the requirements of G.L. c. 184, §§ 31-34 and the city or town must own any real property interest acquired with community preservation monies. Management of the properties may be delegated by the legislative body to the conservation commission, park commission or to a nonprofit corporation created under G.L. c. 180 or nonprofit trust created under G.L. c. 203.

Acquisition of open space – Appropriation of CP funds to a conservation fund established by G.L. c. 40 § 8C is allowable; however, any expenditure of such funds remains subject to the restrictions imposed by the CPA, including the requirement that any land acquired must be bound by the restriction described in G.L. c. 44B, § 12. Therefore, the conservation commission may spend CPA funds only for those purposes that are authorized by both G.L. c. 40 § 8C and the CPA, for example, acquisition of land for open space purposes. To ensure that these requirements are carried out, the CPC recommendation and any legislative body appropriation vote should expressly include these conditions.

Rehabilitation of open space – Expenditures for rehabilitation and restoration of open space (not including lands for recreational use) are not allowable unless the open space was acquired or created using CPA funds pursuant to G.L. c. 44B, § 5(b)(2). For example, funding is allowable for “rehabilitation” of municipal forest land only if the forest land was acquired with community preservation funds. CP funds cannot be used, however, to fund any expenditure that would fall within the CPA definition of “maintenance,” even if the expenditure is required by a forest management plan. G.L. c. 44B, §§ 2 and 5(b)(2). See Part 6 of these FAQs for more information on prohibited CPA expenditures, published in the December 3, 2020 edition of City & Town.

Stay tuned for next month’s City & Town for Part 9 in our FAQ series on the CPA when we will discuss allowable CPA land for recreational use projects. For more information, see Informational Guideline Release (IGR) 19-14.