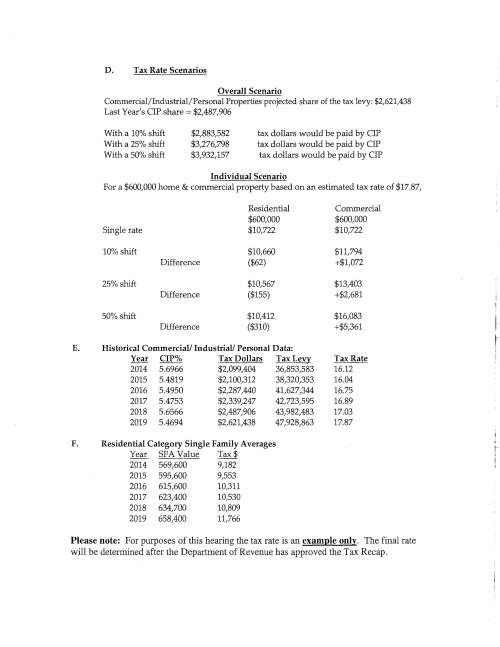

The Board of Selectmen received the report below today from the Assessors for the tax classification hearing that will occur this evening as part of the select board meeting. Towns in Massachusetts are permitted to charge the commercial and industrial taxpayers property taxes at a rate up to 50% higher than the residential rate (called a split tax rate), but Medfield never has.

Medfield’s reality is that because so little of our tax base is other than residential, even if we were to opt for the 50% higher tax rate on commercial and industrial properties, while the commercial and industrial properties taxes would go up by a lot (50%), the home owner would see little change – scant benefit to homeowners, while strong fiscal policy discouragement for any commercial/industrial uses. For that reason Medfield has always kept a single tax rate. See a PDF of the analysis here – 20181127-Assessors-tax classification hearing analysis

Accepting that developing differential tax rates would not provide benefit to home owners because there is a small industrial base, a plan to address the lack of such a base needs to be developed and communicated to residents.

LikeLike

As a new selectman, my first search was for businesses that wanted to locate in town, and when that did not seem a likely result, I have turned to having a town policy of building housing that this revenue positive to the town.

We do know that people want to live in town, but mainly not build businesses here. Therefore, the town can make money and reduce our taxes by building the right kind of housing, such as Old Village Square (42 units paying over $600K/year in taxes, with one school child the last time I heard) or the two Larkin brothers projects (Glover Place off North Street and Chapel Hill on Hospital Road, again both with few school children).

Search my blog for the analysis that Kathy McCabe, the consultant to the Medfield State Hospital Master Planning Committee, did of the potential taxes to the town from leasing the land to build 42 units of senior housing on the town owned lot 3 on Ice House Road versus leasing to a commercial facility, and the town netted about double the taxes from the residential use over the sports complex.

I think that many of the friendly 40B projects that we are currently allowing in order to be in safe harbor, will be revenue positive. Statistically, we will likely average about 1.5 school children per in single family houses, while we will likely average 0.15 school children per unit in multifamily housing. So multifamily housing may be revenue positive for the town.

Additionally, the town is mainly single family homes, so we really do not need any more single family homes, while we do not have a sufficient variety of other housing opportunities for residents, especially for seniors. Current proposals in the pipeline will assist at filling in that gap:

8 units on North Street (two developments)

36 units on Dale Street

16 units on Adams Street, age restricted

42 units at the Rosebay, age restricted

56 units at The Legion site

Such diversification of the tax base can only accomplish so much with respect to reducing our individual tax bills. The other issue with which we need to deal is the town’s willing to spend, witness our vote at the last annual town meeting (ATM) to increase our tax bills by about 10%, over the objections of the Board of Selectmen and the Warrant Committee.

LikeLike